NEWSLETTER

NEWSLETTER

Record-to-Report (R2R) is a critical finance management process in corporate finance, which focuses on collecting, processing, and delivering accurate financial data.

This process encapsulates everything from recording financial transactions to the preparation and reporting of financial statements and performance reports that stakeholders use to make key decisions.

For businesses, R2R is not merely a regulatory or accounting formality but serves as the backbone of strategic financial planning and analysis. It offers a mirror into the organization’s financial health, enabling informed decisions that drive growth, sustainability, and compliance with regulatory standards.

Understanding R2R in its entirety, therefore, is not merely for accountants or financial analysts but is crucial for everyone within an organization.

The Concept of Record-to-Report

The Record-to-Report (R2R) cycle is the financial heartbeat of an organization. It’s a comprehensive framework that transforms raw financial data into meaningful, actionable insights.

The R2R cycle includes these key components:

- Data Collection: The foundation of R2R, where all financial transactions are accurately recorded.

- Data Processing: Transactions are classified, sorted, and recorded in the appropriate accounts.

- Consolidation: Data from various sources and subsidiaries is combined to present a unified financial status.

- Reconciliation: Ensuring that all financial data is accurate and consistent across reports.

- Reporting: The creation of financial statements and reports that reflect the company’s financial health.

- Analysis: Interpreting data to provide insights for strategic decision-making.

- Closing: Finalizing reports and closing the books for the period.

The Need of Record-to-Report

The R2R plays a pivotal role in managing finance within a business. It serves several purposes –

1. Enhanced Decision-Making Capability

The R2R process is pivotal for creating accurate financial statements, which serve as the bedrock for strategic decision-making across various levels of the organization.

- For Internal Stakeholders:

- Performance Evaluation: Enables leaders to assess financial health and operational efficiency against predefined goals and benchmarks.

- Strategic Planning: Facilitates the formulation of actionable strategies to address gaps, optimize performance, and capitalize on opportunities.

- For External Stakeholders:

- Investment Decisions: Provides investors and external parties with essential data to evaluate the organization’s financial viability and potential for growth.

- Transparency and Trust: Enhances stakeholder confidence through clear, reliable financial reporting.

2. Regulatory Compliance and Accuracy

Adherence to financial regulations is non-negotiable, and the R2R process ensures organizations stay compliant while maintaining the accuracy of their financial reports.

- Standardized Reporting Framework: Offers a consistent method for capturing and validating financial data, crucial for meeting diverse regulatory requirements.

- Risk Mitigation:

- Compliance Risk: Reduces the likelihood of non-compliance with industry and geographical financial reporting standards.

- Financial Risk: Minimizes errors in financial reporting, thereby avoiding potential fines, legal consequences, and reputational damage.

3. Tax Reporting and Strategy

The R2R process is instrumental in providing the detailed and organized financial information necessary for effective tax management.

- Tax Liability Assessment: Enables accurate calculation of tax obligations, ensuring compliance with tax laws and regulations.

- Strategic Tax Planning: Identifies opportunities for tax optimization and savings, enhancing fiscal efficiency.

In conclusion, the R2R process is not just a procedural necessity but a strategic tool that supports critical areas of business management—from making informed decisions and ensuring compliance to optimizing tax strategies.

The Process of Record-to-Report

Let’s delve into the Record-to-Report (R2R) process and journey through its sequential steps, exploring it’s pragmatic application in business context.

In integrating software solutions like ERPs and accounting automation tools into the R2R process, businesses can achieve significant gains in efficiency, accuracy, and strategic insight. As we advance, the role of technology in R2R will only grow, transforming financial reporting from a mere statutory requirement into a strategic asset for business decision-making.

Manual R2R Process

Some freelancers, startups, and small businesses navigate the Record-to-Report (R2R) process without the sophisticated infrastructure of ERP or dedicated accounting software, especially in their early stages. This approach is often driven by cost considerations, simplicity, and the initial lower volume of transactions.

- Data Collection: Manual entry into spreadsheets or simple accounting tools like Excel. Transactions are recorded in a ledger format noting the date, amount, and payment method, with separate sheets for sales, expenses, assets, and other financial events.

- Data Processing: Categorization and recording of transactions are manually managed at the time of data collection. The business owner or a designated employee reviews each transaction, determining its nature (e.g., revenue, expense, asset purchase) and recording it accordingly in the appropriate ledger.

- Consolidation: In very small businesses or startups, consolidation might not be necessary if the company operates from a single location and doesn’t have subsidiaries. However, if needed, consolidation is done manually, often by preparing a master spreadsheet that aggregates financial data from various sources.

- Reconciliation: Reconciliation involves manually checking the records against bank statements and receipts. This can be time-consuming but is crucial for ensuring accuracy in financial reporting.

- Reporting: Financial reports are manually compiled, either by employing a freelance consultant at the end of each quarter or by using templates in Excel or Word. This step requires a good understanding of financial principles to ensure that reports such as income statements, balance sheets, and cash flow statements are accurately prepared.

- Analysis: Analysis may be less formalized in smaller operations without dedicated software. Business owners or managers might review financial reports to identify trends, profitability, and areas for cost savings, relying on their intuition and experience rather than sophisticated analytical tools.

- Closing: The closing process is manual, with a checklist to ensure all financial activities for the period have been recorded and reconciled. This might include confirming all invoices have been issued and paid, expenses recorded, and necessary accruals made.

Operating without an ERP or dedicated accounting software requires meticulous record-keeping and a strong grasp of accounting fundamentals. While feasible for businesses with a very small volume of transactions, as a company grows into an SME (small and medium-sized enterprises), the limitations of manual processes become increasingly apparent, often necessitating a transition to more sophisticated accounting solutions and automation to ensure efficiency, accuracy, and compliance.

R2R Process using accounting software / ERP

For businesses that have moved beyond spreadsheets, the use of standalone accounting software / ERP represents a significant step forward in managing the Record-to-Report (R2R) process. This scenario typically involves more sophisticated financial management than manual methods allow.

Data Collection

The shift to accounting software or ERP systems partially automates the entry of transactions.

- These platforms can directly integrate with bank accounts, point-of-sale systems, and other financial data sources, automatically recording transactions in real time.

- Invoices and other transactions received via email or paper-based receipts require manual entry into the system.

- Custom or irregular financial transactions that do not fit standard templates or categories may need manual intervention to ensure accurate recording.

Data Processing

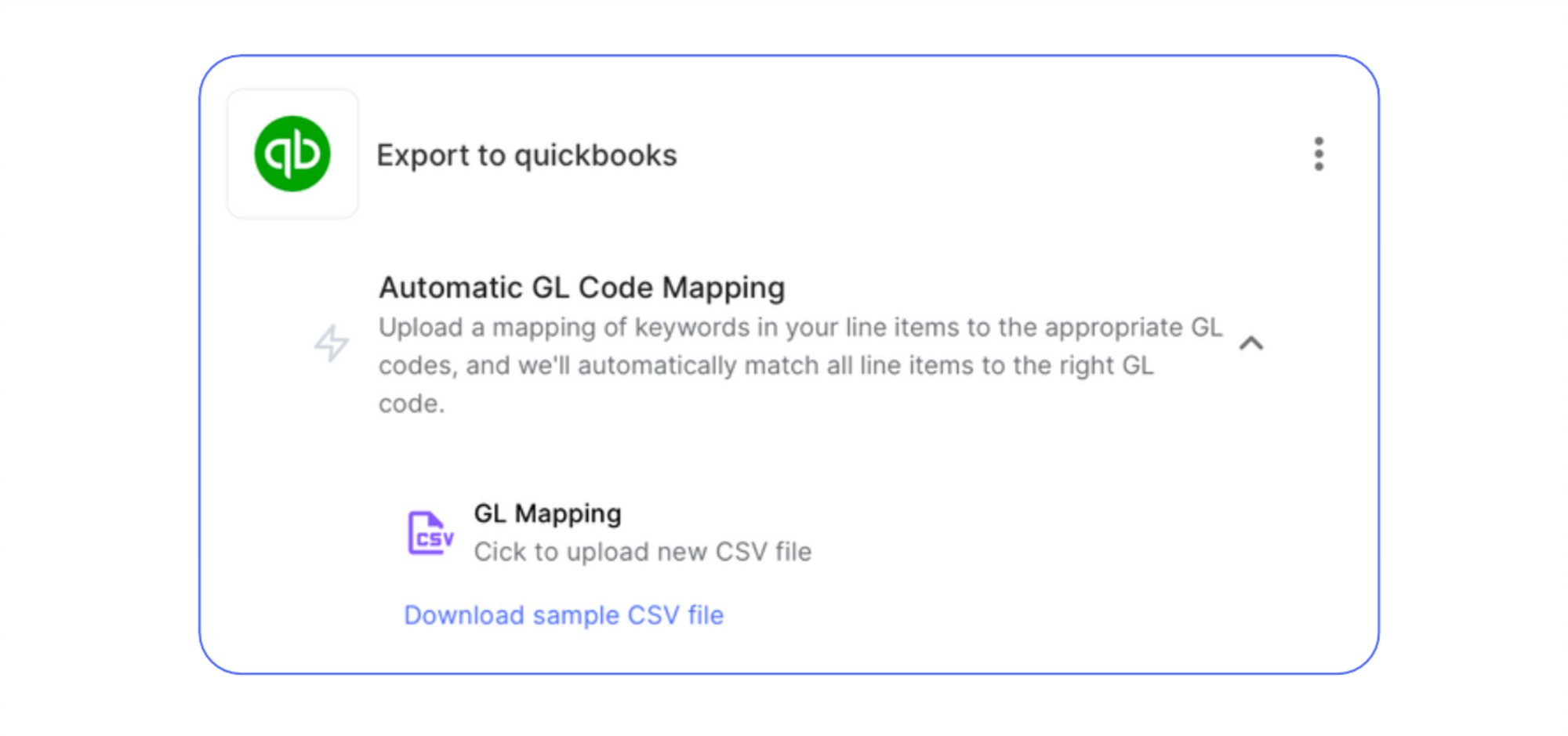

With accounting software or an ERP system, transaction categorization and recording is implemented using a chart of accounts and appropriate GL coding for each financial transaction, which is done manually. The software identifies the nature of each transaction based on the GL code inputted (manually assigned) and allocates it to the correct ledger (expenses, assets, revenue, etc.), significantly reducing manual workload and the potential for errors. Vendor coding can further help to ease categorization.

Everything You Need to Know About GL Codes

GL Codes are codes used to categorize financial transactions. Learn how to set up and assign them, and explore GL code automation with Nanonets.

Consolidation

For businesses with multiple departments or subsidiaries, accounting software and ERP systems facilitate the consolidation process.

These systems can handle data from diverse sources, automatically consolidating it into a unified preset of accurate financial statements, ready for analysis and reporting.

Reconciliation

Some features in accounting software and ERP systems aid the process, with some manual effort required.

- Need to populate data of bank transactions in the ERP / accounting software using manual entry.

- Matching transactions recorded in the software against bank statements may reveal unmatched items due to timing differences or errors, necessitating manual investigation and resolution.

Reporting

Generating financial reports becomes straightforward with accounting software or ERP systems.

They can automatically compile financial statements based on the recorded transactions, adhering to the applicable financial reporting standards.

Users can often customize report templates to meet specific requirements without extensive manual effort.

Analysis

The availability of real-time data paired with comprehensive reporting and analytics enhances the capacity for informed decision-making.

While these systems provide basic analytical tools that offer insights into financial performance, trends, and other key metrics, deeper analysis may still require human interpretation.

Closing

The closing process benefits from the structured approach provided by ERP systems, which offer checklists and workflows.

However, manual interventions are frequently necessary to adjust journal entries, review and approve reconciliations, and ensure that all financial activities are accurately captured.

Complex or unusual transactions at the end of the reporting period, in particular, may require detailed manual review to ensure proper recording and classification.

Automated R2R Process Using Nanonets and Accounting Software

Integrating accounting software or ERP systems with accounting automation software like Nanonets revolutionizes the Record-to-Report (R2R) process, offering unparalleled efficiency, accuracy, and actionable insights for financial management.

Data Collection

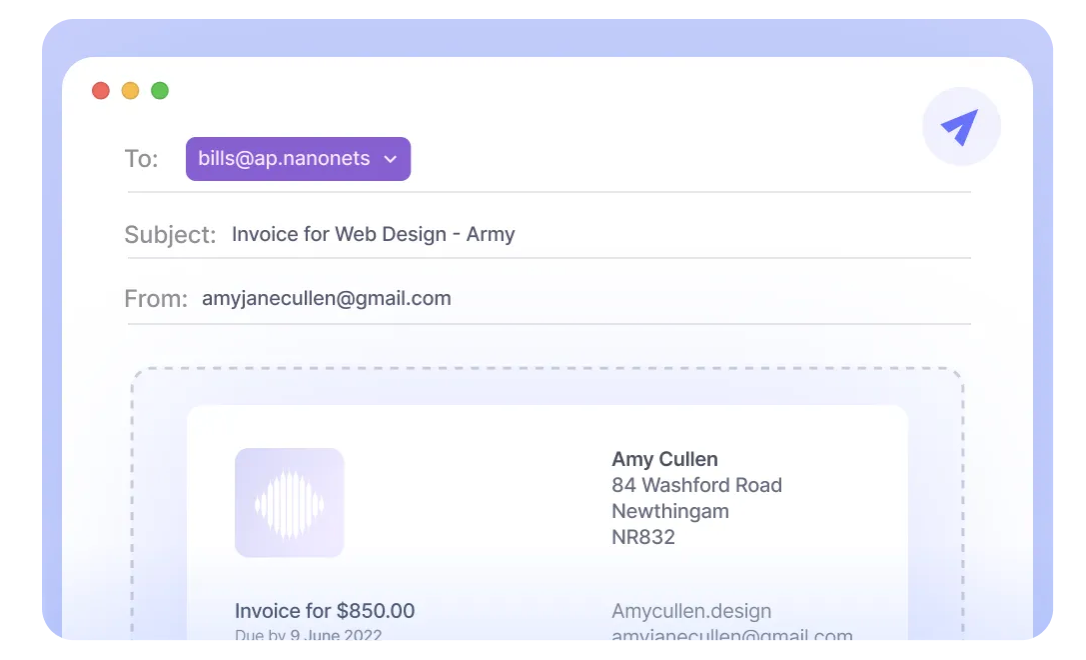

Through the integration with AP automation platforms such as Nanonets, the collection and entry of financial data become fully automated, leveraging OCR and ai technologies.

Every piece of financial information is automatically collected from it’s origin (invoices, receipts, emails, POS systems, bank statements) and processed as soon as it arrives, ensuring a seamless flow of data into your financial systems.

With ai-powered data extraction boasting accuracy rates exceeding 99%, the reliability of your financial data is significantly enhanced, saving countless hours and transforming the workplace atmosphere.

The real-world impact is profound: Imagine your team redirecting their focus from tedious data entry to engaging in more strategic, high-value tasks.

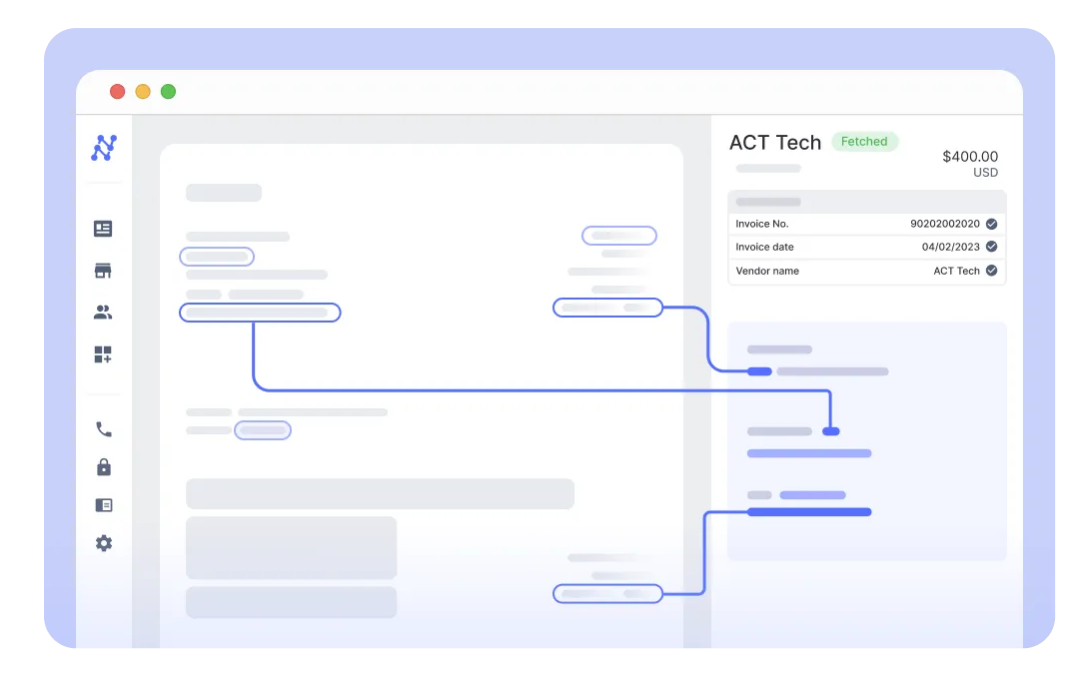

Data Processing

Once data is collected, it’s automatically processed and coded into your accounting software or ERP system in real time.

The traditionally labor-intensive tasks of coding General Ledger (GL) entries are now effortlessly handled by advanced ai, including Natural Language Processing (NLP) and Large Language Models (LLMs).

This automation not only speeds up data processing but also minimizes errors, freeing your finance team to apply their skills and expertise where it matters most.

Consolidation

Nanonets can be configured to execute post-processing steps, adeptly managing complex scenarios such as intercompany transactions and multi-currency operations. This ensures that the data feeding into your ERP or accounting software is consistently clean and accurate.

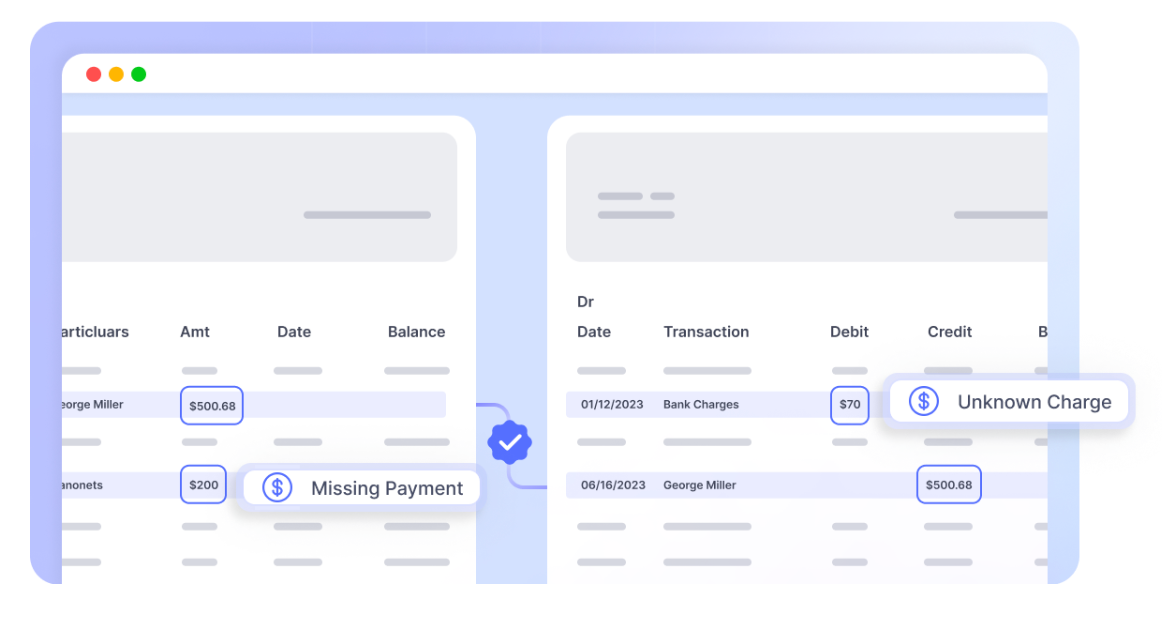

Reconciliation

Nanonets can automatically import your bank statements and match transactions against bank statements, flagging any inconsistencies for human review, thereby improving accuracy and reducing the risk of financial discrepancies.

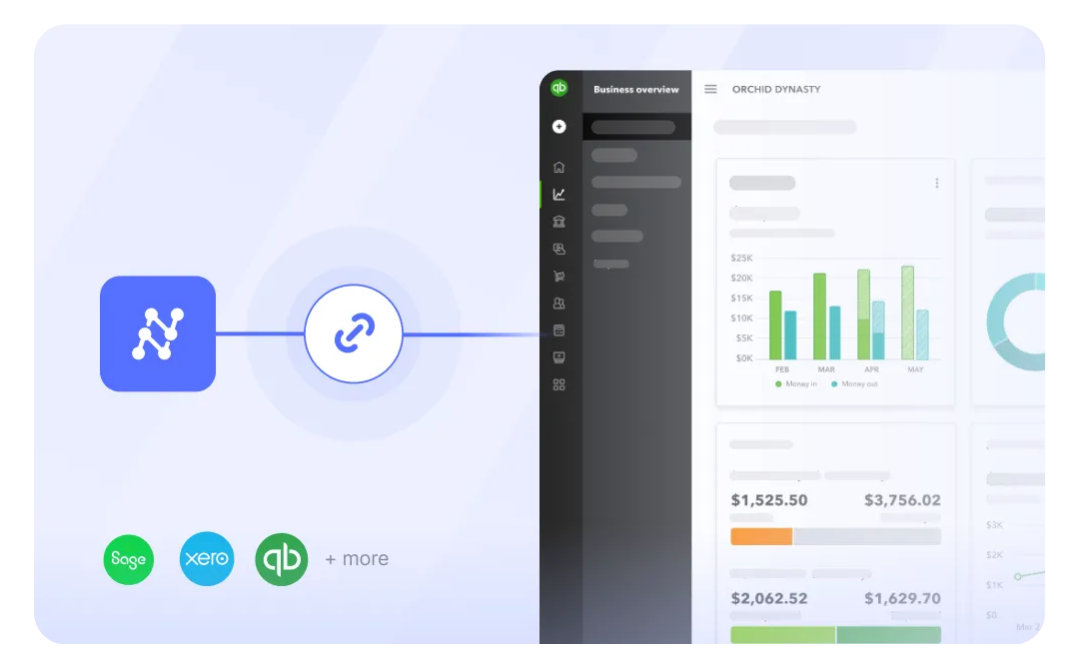

Reporting, Analysis and Closing

With transactions reported instantaneously as they occur, decision-makers gain access to up-to-the-minute financial data.

This agility in reporting facilitates more informed and timely business decisions.

Furthermore, the streamlined and automated workflows considerably reduce the time and effort required for closing the books, enhancing efficiency and reducing the potential for errors.

The integration of automation software like Nanonets with accounting or ERP systems does not just alter the R2R process; it revolutionizes it. By automating tedious manual tasks, enhancing data accuracy, and providing real-time financial insights, businesses can not only optimize their financial processes but also leverage strategic insights to drive growth and efficiency.

Further Reading and Resources

The first thing to recognize is that while the overview of the Record-to-Report (R2R) process provided above serves as a strong foundation, businesses actively needs to seek actionable intelligence that can be applied to make their operations more efficient, compliant, and strategically sound. Here’s what’s to look for:

- The Role of Governance, Risk, and Compliance (GRC): How can businesses effectively align their R2R processes with GRC needs?

- Governance in R2R ensures that financial reporting is governed by clear policies, procedures, and standards. It defines roles and responsibilities within the finance team and ensures alignment with broader business objectives.

- Risk Management within R2R focuses on identifying, assessing, and mitigating risks associated with financial reporting. This includes everything from data entry errors to compliance risks with financial regulations.

- Compliance in the context of R2R involves adhering to applicable accounting standards, laws, and regulations. This ensures that financial reports are prepared in accordance with recognized frameworks such as GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards), as well as complying with tax laws and other regulatory requirements.

Six steps for a Successful GRC implementation: https://www.crowe.com/insights/6-steps-for-a-successful-grc-implementation

Integrated GRC: The Key to Better Risk Awareness and Better Performance

Risk and compliance information in the right format, at the right time, and in the right hands is key to organizational success.

- Strategic Implications of R2R: Delve deeper into how R2R insights can be transformed into actionable strategies. For instance, how can trends identified in financial reports inform strategic shifts in business models, investment in new technologies, or entry into new markets? Example –

The digital close

Propelling the R2R process into the digital age

- Case Studies and Real-world Examples: Look for businesses which have successfully optimized their R2R process. This could include examples of cost savings, improved compliance, or strategic pivots based on insights derived from R2R data. Example –

GlaxoSmithKline’s R2R Transformation with Cadency

Learn more from Babak Naraghi, Director of R2R Cadency GPO at GSK, as he discusses GlaxoSmithKline’s financial transformation with Cadency.

- International Standards: What are the implications for businesses operating in multiple jurisdictions?

Conclusion

To sum up, the Record-to-Report (R2R) process is a key part of managing money in businesses, going beyond just following rules to become a crucial tool for success.

By using automation and new tech like ERP systems and tools like Nanonets, companies can work faster, more accurately, and get a clear view of their financial status in real-time.

An efficient R2R process not only makes day-to-day work smoother but also helps in making big decisions, helping companies deal with today’s business challenges more smartly and with better planning.

As we look forward, the role of R2R in business strategy will only increase, making its mastery a key determinant of organizational success.

{kind=link}