NEWSLETTER

NEWSLETTER

The need for automation in the insurance industry is more pressing than ever. According to a recent study by Datos Insights, the insurance industry lags in terms of digitisation, with only 20% automation in underwriting and less than 3% automation in claims processing across sectors. This gap represents a significant opportunity for improvement and cost savings.

Underwriting and claims processing are two key insurance processes that are still handled manually. This results in increased turnaround times and unpleasant customer experiences.

One of the most promising solutions to these challenges is the adoption of Straight Through Processing (STP) in insurance. In the insurance industry, STP translates to automating various processes such as financial credibility assessment, KYC/Identity verification, underwriting, and claims processing.

In this blog post, we’ll explore what STP means in the context of the Insurance industry, the pain points within the industry and the benefits of STP. We will also understand how we can leverage ai-based Intelligent Document Processing (IDPs) tools to automate STP and reduce human dependency in this sector.

So, let’s get started.

What is Straight Through Processing in Insurance?

Straight Through Processing in insurance refers to the end-to-end automation of insurance processes, from initial customer interaction to final resolution, without the need for manual intervention. This automation can be applied to various aspects of the insurance value chain, including policy applications, underwriting, and claims processing.

Let’s explore some specific use cases where STP can make a significant impact:

1. Claims Processing

Claims processing is perhaps the most visible and impactful area where STP can be implemented. Traditional claims processing involves multiple manual steps, from claim submission (First-notice-of-loss or FNOL in certain sectors like vehicle insurance etc.) to assessment, verification, and settlement. With STP, this process can be significantly streamlined.

For example, consider a health insurance claim. A policyholder gets a minor procedure done over the course of a day while being hospitalized. Instead of calling an agent or filling out lengthy forms, they could:

- Use a mobile app to take photos of the hospital admission documents and the bills

- Submit these photos along through a mobile application

- Have an ai system extract relevant details along with authenticity verification

- Get immediate approval and payout if it falls within certain predefined parameters

This entire process could happen in minutes, with minimal human intervention from the insurer’s end.

2. Underwriting for Insurance

Underwriting is a complex process that traditionally requires significant human expertise. It assesses the financial credibility of an individual applying for an insurance policy to help decide whether that person should be insured. It involves multiple sub-processes, which we will cover in the following sections. However, with STP and ai, much of this process can be automated:

- The system collects all relevant data about the applicant (the application form, uploaded IDs, such as, SSN Certificates, Passports, etc. and financial documents)

- There are two important sub-processes in the insurance sector: KYC/Identity Verification and Credit Scoring.

- Uploaded IDs undergo an authenticity check and data extraction, which is cross-verified against an external database for verification.

- Similarly, Tax Forms (depending upon geographic location, for example, Income Tax Returns for India and 1099 and W2 forms for the US among others) and bank statements undergo data extraction and this data is made accessible.

- ai algorithms then analyse this data to assess the risk associated with issuing a loan to a particular individual.

- For straightforward cases that fall within predefined parameters, the system can make an automatic decision on whether the policy should be issued or denied

- For more complex cases, the system can flag them for human review, providing a detailed risk assessment to aid the underwriter’s decision

Pain Points Addressed by STP

The insurance industry faces numerous challenges that hinder its efficiency and customer satisfaction. These pain points span across various aspects of insurance operations, from customer experience and fraud prevention to operational efficiency and regulatory compliance. As the industry evolves in the digital age, addressing these challenges has become increasingly urgent. Let’s look at some of the most pressing issues troubling the insurance sector today:

- Slow Processing Times and Inconsistent Customer Experience:

Traditional manual processes in the insurance sector can take days or even weeks for achieving simple tasks. This leads to inconsistencies in how customers are treated for similar issues. According to this report by Accenture, US$ 170 Bn. in global premiums is at risk of churning by 2027, largely due to poor customer experience.

- Fraudulent Claims:

According to this report by McKinsey, about 5-10% of claims in the property and casualty insurance sector in the Americas and Europe are fraudulent. By simplifying this process with the help of ai, there is a potential for reduction in fraudulent claims.

- Human Error and Scalability Challenges:

Manual data entry within any insurance process, be it underwriting or claims, is prone to errors. A simple mistake in assessing the financial credibility of an individual can lead to policy rejections or exponential payouts hurting the insurance agencies. When a process is manual, it becomes increasingly difficult to scale it without scaling the error rate.

- High Operational Costs:

Moreover, scaling manual processes can lead to high payroll costs within insurers. Since most of these organizations are large-scale enterprises, processing hundreds of thousands of documents per day, a manual workforce supporting crucial processes is not optimal.

- Compliance Risks:

Insurance industry is highly regulated with multiple compliances to adhere to. Not just that, this is an industry that is constantly evolving with policy changes every few months. Manual processes increase the risk of non-compliance with regulations dramatically. This can cause issues with audit and credibility certifications.

Benefits of Automation and Impact on STP

According to a McKinsey Global Institute report, there is a 43% potential for automation in the insurance and finance sectors. As of 2023, this report by Statista says that 14% of insurance firms surveyed were beginning the process of automation in their claims and processing department. But why? Simply because, there is immense savings of resources, an exponential increase in STP of simpler cases and a dramatic increase in efficiency to be realized by leveraging modern-day tools.

1. Increased Efficiency

Automation in insurance reduces manual workflows, speeding up processes such as underwriting and claims handling. For example, automated claims processing can reduce the average cycle time from days to minutes. By eliminating repetitive tasks, employees can focus on higher-value activities, improving overall productivity.

2. Cost Reduction

Automation slashes operational costs by minimising the need for manual intervention and paper-based processes. ai-on-the-future-of-insurance”>McKinsey estimates that 30-40% of traditional insurance processes can be automated, leading to potential cost savings of 20-30% in administrative expenses. This also reduces the cost per claim, contributing directly to the company’s bottom line.

3. Enhanced Customer Experience

Automated systems enable insurers to offer faster and more accurate services, such as instant policy issuance and quick claims approval, which improves customer satisfaction. According to a PwC study, 41% of insurance customers would switch providers due to poor digital experiences, while automation can enhance responsiveness and reduce complaint rates. Real-time updates and seamless interactions drive higher retention and brand loyalty.

4. Fraud Detection

Automation aids in identifying and flagging suspicious patterns through data analytics and real-time monitoring. Fraud detection systems can reduce fraud-related losses by up to 40%. Insurers using automated fraud detection report an improvement in accuracy and speed, as they can process vast amounts of data far beyond human capacity.

The impact of these benefits on STP is significant. As more processes become automated, the percentage of transactions that can be processed straight through increases. This creates a virtuous cycle: more automation leads to more data, which leads to better ai models, which in turn enables even more automation.

Implementing Straight Through Processing in Insurance

We have discussed the positive impact that STP can have on the insurance industry, but the question remains how to implement it? There are two popular methods Insurance companies go about this:

- Using ai-based Intelligent Document Processing (IDP) platforms

- Using Conversational Process Automation (CPA) platforms

<h3 id="method-1-workflow-automation-using-ai-based-idps”>Method 1: Workflow automation using ai-based IDPs

Workflow automation using ai-based Intelligent Document Processing (IDP) is a cornerstone of STP in insurance. This method leverages artificial intelligence to automatically extract, classify, and process information from various document types, such as claim forms, policy applications, and supporting documents.

ai-based IDPs can handle both structured and unstructured data, significantly reducing manual data entry and associated errors. By automating document-heavy processes, insurers can dramatically speed up processing times, improve accuracy, and enhance overall operational efficiency.

This technology enables insurers to process a higher volume of transactions with fewer resources, leading to cost savings and improved scalability. Moreover, ai-based IDPs continuously learn and improve over time, adapting to new document formats and becoming more accurate with each processed document.

Method 2: Conversational Process Automation

Conversational Process Automation (CPA) in insurance STP focuses on using ai-powered chatbots and virtual assistants to guide customers through various processes, with a particular emphasis on claims processing and triaging.

This method combines natural language processing with robotic process automation to create an intuitive, conversational interface for customers. In claims processing, CPA can guide claimants through the entire process, from initial notification to final settlement, asking relevant questions and providing real-time updates. For claims triaging, the system can automatically categorise and prioritise claims based on the information provided, routing simple claims for immediate processing while escalating complex ones to human adjusters.

This approach not only speeds up the claims process but also improves customer satisfaction by providing 24/7 service and instant responses. Additionally, CPA can handle policy inquiries, quote requests, and simple policy adjustments, further streamlining insurance operations and enabling true STP across multiple touch-points.

<h2 id="ai-based-idps-for-stp-in-insurance”>ai-based IDPs for STP in Insurance

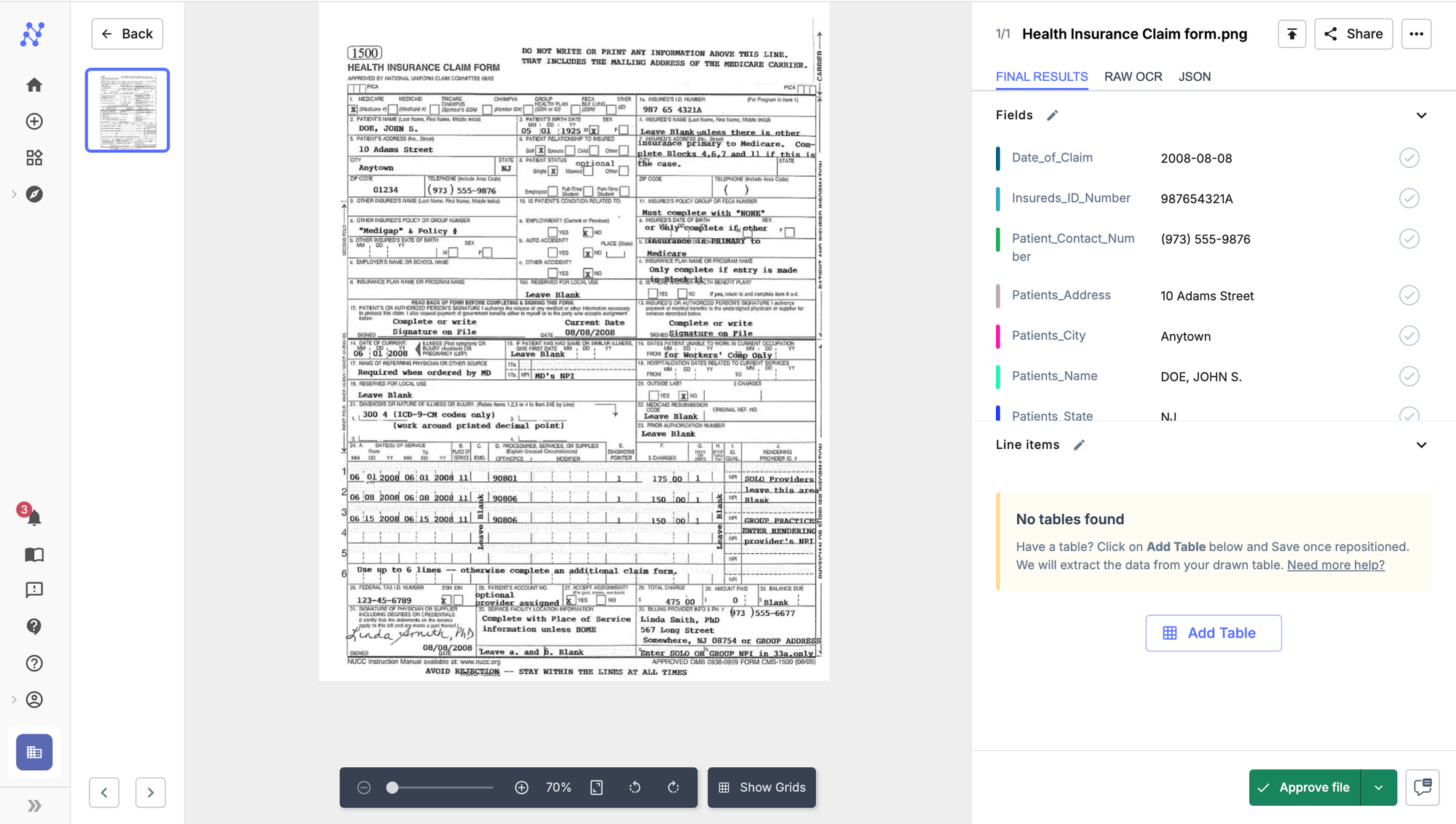

In this section, we will take a deeper look at how exactly one can implement STP for insurance processes in their organization by taking a specific example. We will see how to process a health insurance form using Nanonets.

So, let’s get started.

Step 1: Visit the Nanonets platform (app.nanonets.com)

Step 2: Click on “Workflows” on the left panel > “Zero-training extractor”

Zero-training extractor: Using the zero-training extractor, you can deploy an OCR model for any document, be it a Patient ID card, Hospital bill, claim form, financial statements or any other document that is crucial to the process you want to automate.

Step 3: Now, all you need to do is enter the label names. For instance, in this health form we have taken:

- Patient’s name

- Patient’s address

- Patient’s city

- Patient’s state

- Patient’s zip code

- Insured’s ID number

- Date of claim

- Insurance type

In case of any tabular fields, you can flip over to the “table headers” section from the top.

Step 4: That’s it. Click on “Continue” and upload your file to manually test it out.

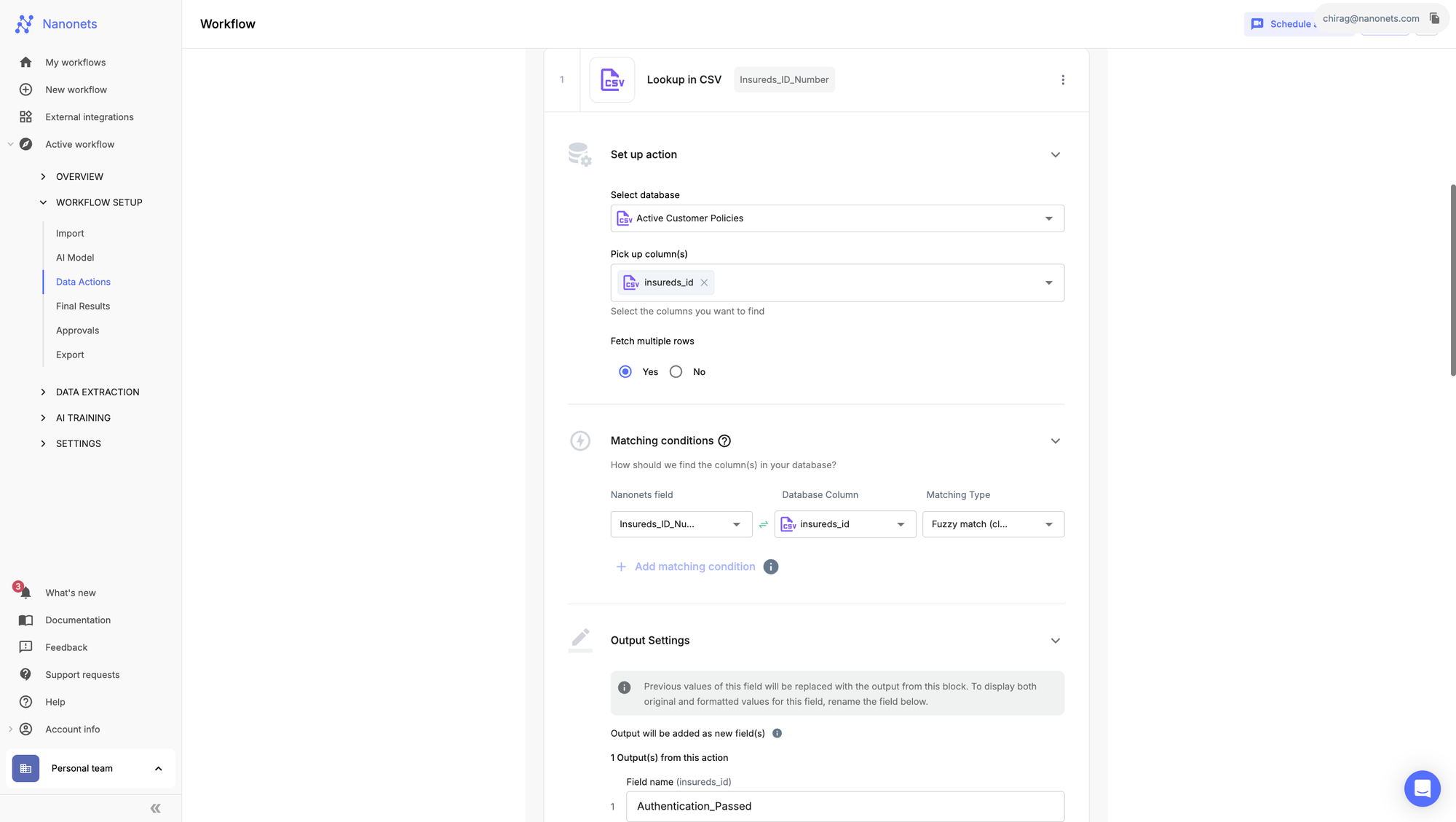

Step 5: Navigate to the “Workflow” section on the left panel > “Data Actions” section.

1. Using the lookup capability, we can set up a workflow to “fuzzy match” the Insurance policy number against your organisation’s records. In case of a match, we can have a new field populated that says, “authentication passed.”

2. Alternatively, let’s say you want to ensure that the policy was active when the claim was made. You could “fuzzy match” the date of claim against the policy period stored in an external database.

These are just a few examples of the “custom actions” Nanonets can perform including mathematical functions, formatting actions and many more.

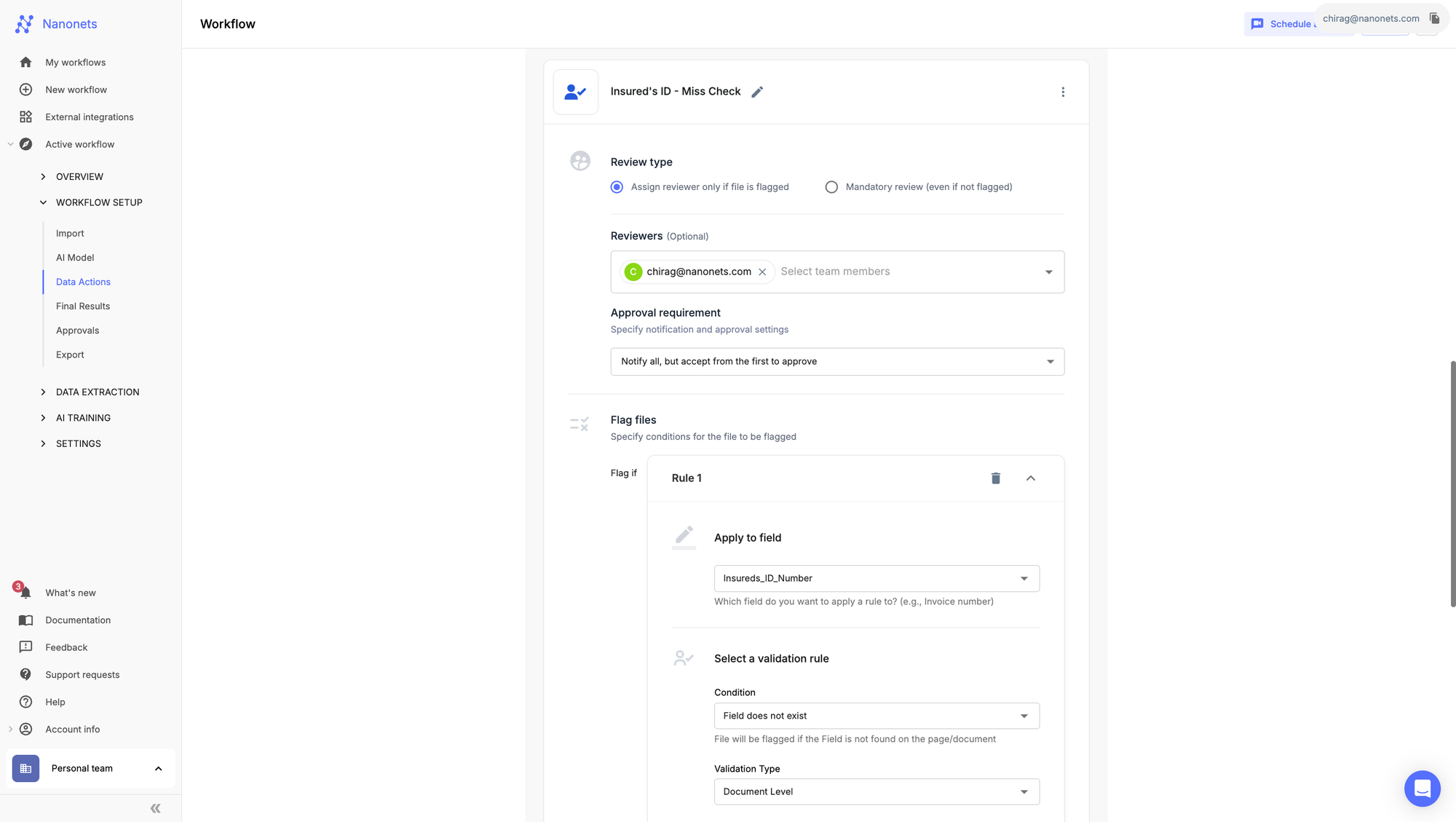

Step 6: Navigate to the “Approvals” section on the left panel under “Workflow setup”

You can define custom logic actions in the “Approvals” section that flags a particular file for manual review. You can create a condition that flags a file in case the Insured’s ID is missing and notify an agent for reviewing a particular file.

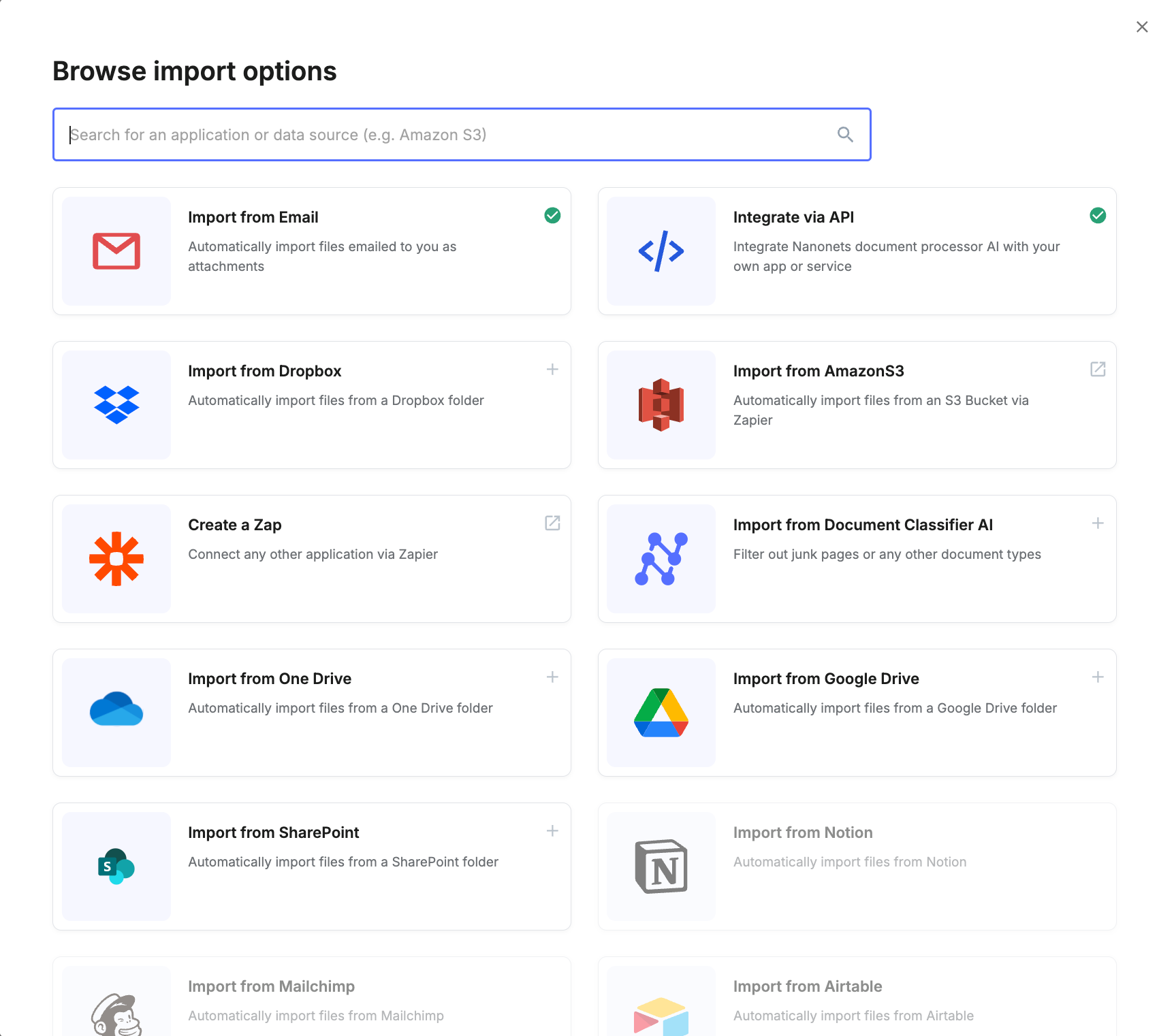

Step 7: Navigate to Import and Export section under “Workflow setup”

1. With a variety of automated import and export options, this entire process can be automated end-to-end. You can import the files, in this case, claim forms from email inboxes, cloud storages, like, G-Drive, Dropbox, One drive, or even databases, like amazon S3. There is always an option to import files using the API endpoint.

2. Similarly, you can export to third-party software. Popular options include ERPs like Salesforce, etc. or databases, like, amazon S3. There is always an option to export the data into internal systems via API endpoints for assessment.

So, there we have it! An example of how one can leverage all the features that Nanonets offers to successfully implement STP in Insurance processes. The best part is that this is completely customisable and can be tailored to different processes and document types in a secure and user-friendly manner.

{kind=link}