NEWSLETTER

NEWSLETTER

Bernstein analyst Toni Sacconaghi generated some headlines on March 27 when he lowered his price target for tesla (NASDAQ:TSLA) at $120, down 30% from its price at the time.

Blaming an outdated model line and increased competition, he said: “Tesla's stock price remains high on almost all valuation metrics compared to traditional and faster-growing auto (makers), and also appears expensive relative to its reduced growth expectations when compared to technology companies.

But what's new? It has been expensive for as long as I can remember, which is why I never bought the stock.

The big problem

However, Sacconaghi's comments highlight (what I believe) is the fundamental problem. Is Tesla a car manufacturer or a technology company? I believe that only when this is resolved will it be possible to make an informed investment decision.

Chart by TradingView

The chart below shows the company's price-to-earnings (P/E) ratio over the past five years. Although it has fallen recently, it is still higher than that of the tech giant. Apple. FordThe P/E ratio is 70% lower than Tesla's.

Personally, I think Tesla is a car company. Yes, its autonomous driving technology could revolutionize the industry. But other major manufacturers, including Ford, are developing their own versions. Tesla's range of all-electric models sets it apart from most, but its technology is not as unique as some might think.

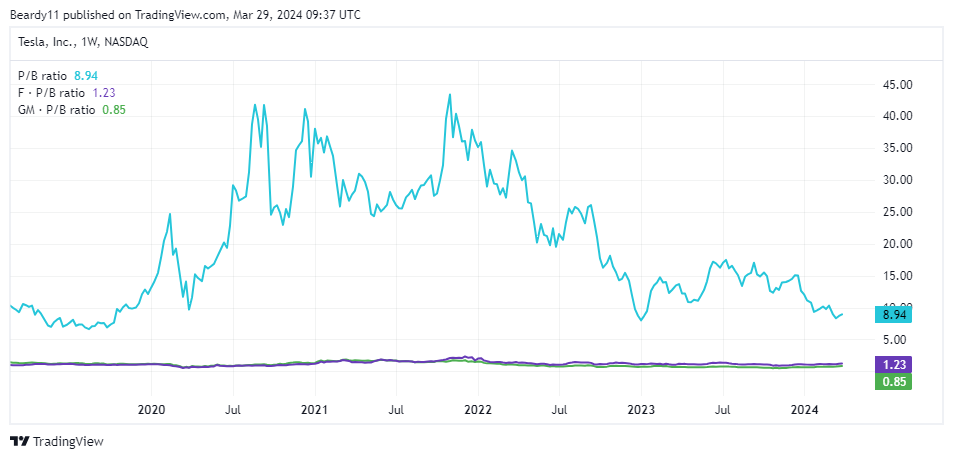

If I'm right, then the stock is significantly overvalued. And if we look at its balance sheet, the disparity between its stock market valuation and its underlying value is even starker. It has a price-to-book ratio of 8.9, which eclipses that of Ford (1.2) and General Motors (0.9).

Chart by TradingView

Major challenges

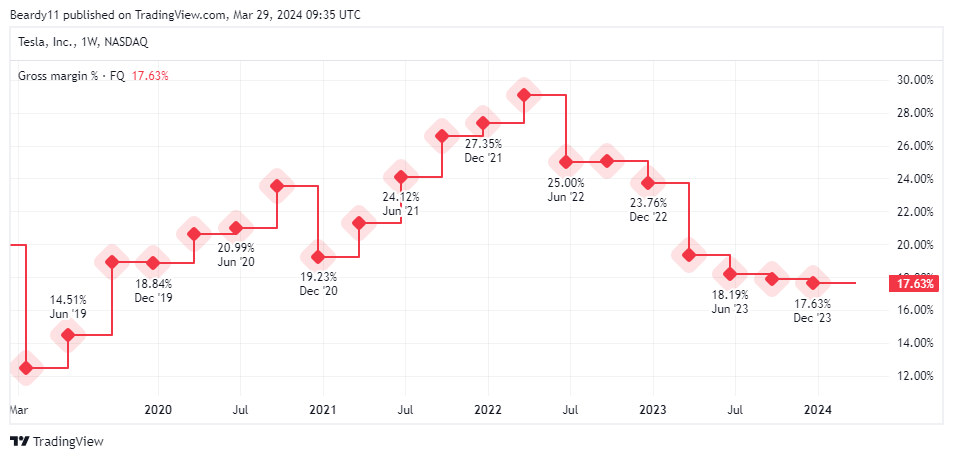

In the face of increased competition, the company has embarked on a series of price cuts. And as shown below, these have hurt their gross margin.

Comparing December 2023 to two years earlier, its automotive margin has fallen 9.8 percentage points. On a $50,000 car, that's $4,900 less profit. Multiply this by 1.8 million vehicles (the number it sold in 2023) and the profit loss becomes $9 billion.

Chart by TradingView

And sales for the first quarter of 2024 are 8% lower than those of the same period in 2023.

A more positive vision

This all sounds pretty bleak, but Tesla has proven critics wrong many times before.

And it's easy to overlook that the Model Y was the best-selling car of 2023. This includes those with gasoline and diesel engines. The company also regularly tops brand loyalty surveys.

I'm also intrigued by Elon Musk's recent interview with Don Lemon. When asked about the new version of the Roadster he said it would be a collaboration with SpaceX, and would incorporate “rocket things”. She went on to describe him as “something that has never existed before” and “not even really a car”with drive-by-wire technology. If that wasn't enough, Musk claimed that he will accelerate from 0 to 60 in less than a second. I can not wait!

It is also true that Sacconaghi's opinions are not shared by everyone. According to CNN, of the 51 analysts covering the stock, 17 rate it a “Buy,” 24 say a “Hold,” and 10 advise a “Sell.” Their price targets range from $68 to $320.

But despite its recent decline, I still think the stock looks expensive, so I don't want to invest right now.

{kind=link}