NEWSLETTER

NEWSLETTER

During the past year, Tesla (Nasdaq: TSLA) has doubled its value. But while this 100% growth is incredible, has the tide turned? Tesla's shares have crashed 22% from where he was just a week before Christmas.

For a company with a market capitalization north of billions of dollars (still), it is a great fall. Is this a purchase opportunity for me, or just the beginning of a quick descent road for Tesla shares?

What to look here

I don't know where the part will go here. No one does. But some things make me nervous about whether the business deserves that assessment (or something like that).

First is the company's car business. After years of strong growth, sales volumes last year decreased (although only slightly).

But the market in general continues to grow. Tesla is increasingly surpassed by rivals as Byd. So while the company total Income grew last year (and are substantial) that growth was small.

Created using tradingView

Even if the car business is established, or see that sales fell this year, which is a giving risk, Tesla has more than one chain in its arch.

He has used his energy storage experience to build a business in that field. It is expanding rapidly and I see strong growth opportunities.

But surely the recent price of Tesla shares cannot be justified only by the automobile business and the energy storage opportunity? I think Wall Street has been taking into account a great cousin for the potential hung by two things: autonomous taxis and robotics.

A difficult atmosphere and be more difficult

Tesla has good opportunities in both areas. But they also do multiple competitors. Alphabet The Waymo subsidiary is already being advanced to Tesla to implement autonomous taxis.

In any case, the business model for that market remains to be seen. If it is too full, players can compete in the price and convert autonomous taxis into a money well, not a money manufacturer. Super It is now profitable, but for a long time it burned effective as if it weren't anyone's issue.

Also in Robotics, Tesla is looking at a field full of people. The business model has not yet been tested, but that I am not clear that Tesla has a unique competitive advantage to distinguish it from other robotics manufacturers.

Things could get worse

If we ignore the assessment for a moment, I see a lot that I like Tesla. While the automobile business seems that it can be without strength for now, it is still huge and simply keeping current sales should be enough to earn serious money.

The energy storage business is growing well and Tesla has a great experience. Other companies, such as autonomous taxis, can be seen as potential growth drivers.

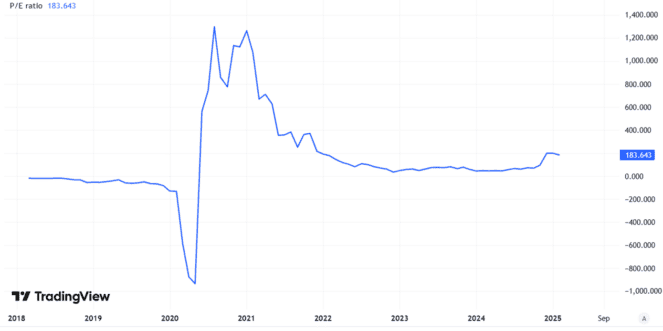

However, as an investor, I cannot simply ignore the valuation. Tesla's shares are sold in a price / profits ratio of 184, which seems very expensive to me. Of course, for a long time it seemed expensive.

Created using tradingView

But having been expensive in the past does not mean that being expensive now is equal to a reasonable price.

The growth prospects in the Tesla automobile business seem worse than before. Other companies such as autonomous taxis are interesting opportunities at this time, but not proven companies.

I think that Tesla's actions looks a bad overvalued and have no plans to buy.

(tagstotranslate) category. Investing

{kind=link}