Image source: Rolls-Royce plc

He Rolls-Royce (LSE:RR) share price has risen almost 200% since October 2022. This is partly due to the recent increase in revenue, as shown in the chart below:

However, I wanted to get a clearer understanding of what management plans to do to maintain such strong share price performance in the future.

Keen Rolls-Royce fans will know that there is a new CEO leading the ranks. Let's see what Tufan Erginbilgiç has in store for shareholders.

Future plans

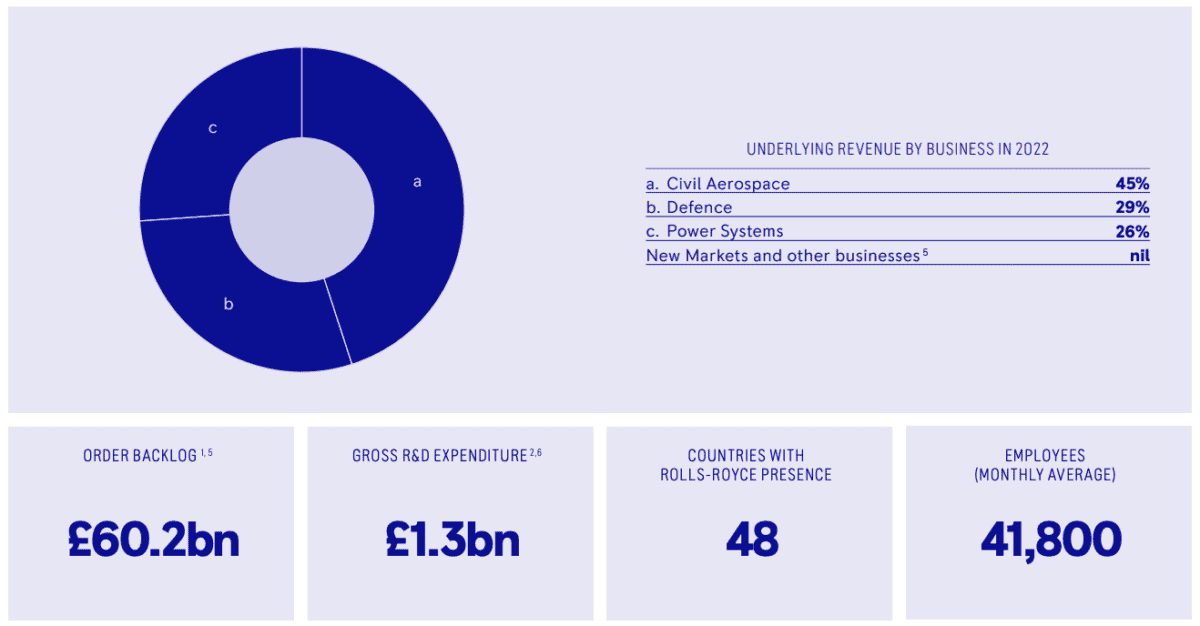

Below is an overview of the business as presented in its 2022 annual report:

The company has some specific future plans worth mentioning.

Firstly, Rolls-Royce is developing a nuclear reactor to place on the Moon, funded by the Space Agency with £2.9 million.

Second, the organization is re-entering the narrowbody aircraft engine market. Its UltraFan technology will focus on sustainability and fuel efficiency.

I think it's important to note that there are significant risks if both projects are successful.

Both have significant regulatory and technical hurdles to overcome, for example.

More specifically, the lunar reactor will face financing and security risks, and the UltraFan will face market competition and demand factors.

The path of Erginbilgiç

A former BP executive, new CEO of Rolls-Royce from 2023, takes the bull by the horns.

It has a financial focus and seeks to improve previous financial instabilities. It also announced layoffs of between 2,000 and 2,5000 employees in an effort to increase efficiency.

As a result, the company saw a five-fold increase in operating profit in the first half of 2023.

When I read about these measures, I am eerily reminded of Musk's acquisition of Twitter. Don't get me wrong, the two situations couldn't be more different in many ways.

However, the drive toward efficiency and an efficient management style has perhaps become popular.

A closer look at finances

I've reviewed Rolls-Royce before. One thing I noticed is that, to me, the fact that the stock price has shot up so high so quickly is not justified by the financials.

For example, although revenue has increased since 2021 after the company was hit hard by the pandemic, it has a lot of debt on its books.

In 2019, during the pandemic, debt reached £5.7bn and rose to £7.8bn in 2021. To put that in perspective, the company had just £3.5bn of debt in 2017.

This worries me as a potential investor.

The company's forward price-to-earnings ratio is also 26. That considers the current share price divided by forecast earnings per share. It ranks in the bottom 25% of 56 aerospace and defense companies in this metric.

Not for me

In my opinion, this is a company that doesn't look too attractive right now.

I think shareholders are driving up the stock price due to premature expectations.

This one is on my watch list because I love studying what's going on here, but I won't be adding it to my portfolio anytime soon.

{kind=link}