NEWSLETTER

NEWSLETTER

Image source: Getty Images

Looking for the best growth stocks to buy in the New Year? Here are two of my favorites.

I put my money where my mouth is and bought them for my own wallet.

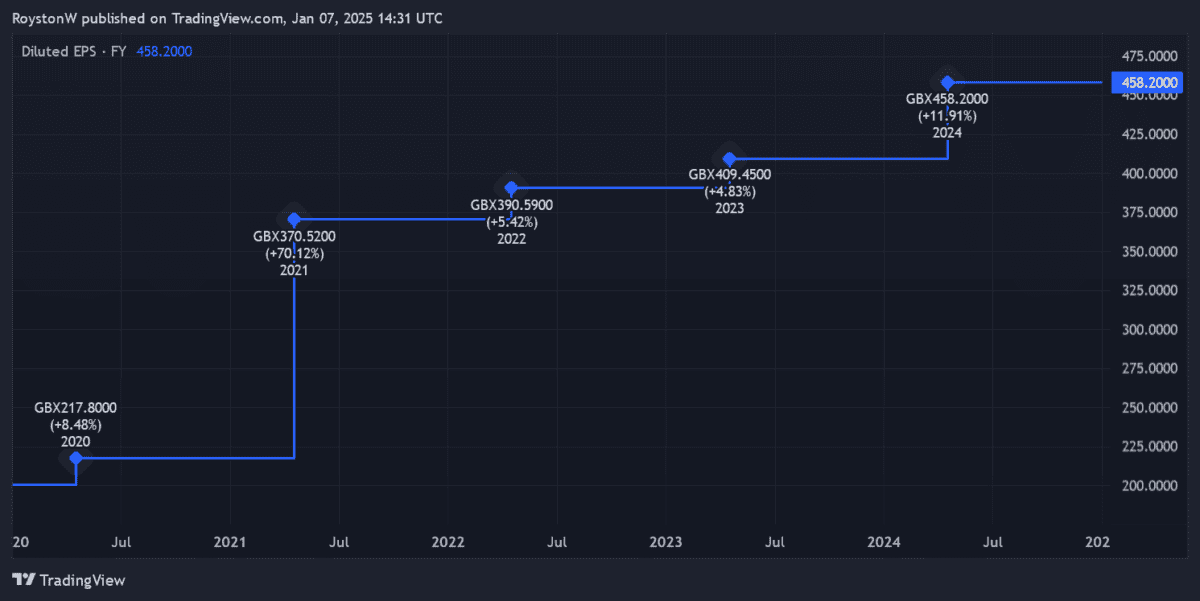

Games workshop

Last year was a milestone for the board game giant. Games workshop (LSE:GAW) when it entered the FTSE 100 for the first time.

Profits here have grown steadily and at a rapid pace in recent years, as the chart below shows. Tabletop war games are not everyone's cup of tea. But it's growing rapidly as global interest in fantasy increases and board games in general enjoy a renaissance.

Through your war hammer product line, Games Workshop is at the forefront of this booming industry. And their goal is to enter the mainstream by releasing film and television content with amazon in the coming years.

It's a move that could boost sales of its traditional gaming systems. and create huge royalty income in its own right.

Meanwhile, profits look set to continue rising strongly as new products come off the shelves and the company increases its store space around the world. The late November trading update underlined its continued trajectory, predicting pre-tax profits of at least £120m in the six months to December 1, a 25% year-on-year rise.

This supports the City's predictions that annual profits will grow by 7% this financial year (to May 2025). Earnings are also forecast to rise another 5% next year.

Games Workshop's strong prospects are reflected in its high price-to-earnings (P/E) ratio of 27.2 times. While I think the company is worthy of this premium valuation, it means its stock could plummet if any setbacks occur.

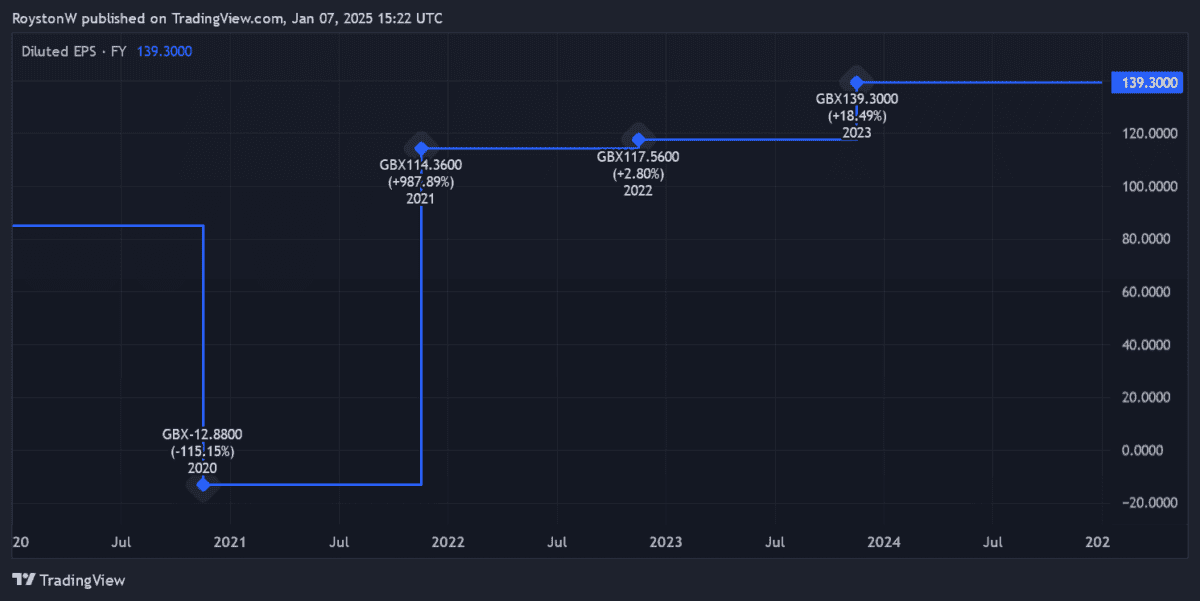

Greggs

Pandemic aside, Greggs (LSE:GRG) has also enjoyed impressive earnings growth in recent years. This is largely due to an expansion strategy that has boosted sales by around three-quarters since 2019.

By 2024, city analysts believe that FTSE 250 The company's profits increased 8% year over year. They predict further substantial growth (7% and 8%) in 2025 and 2026.

This is perhaps not surprising given Greggs' commitment to continue increasing its store floor space from current levels of around 2,560. It planned to open between 140 and 160 new outlets in 2024 alone, and plans to have 3,500 company-run and franchised outlets up and running in the coming years.

Competition in the takeaway food market is intense and remains a threat. But Greggs' recipe of offering generational favorites (like sausage rolls and donuts) at attractive prices is helping it successfully overcome this pitfall. The latest financial data showed that sales increased by 12.7% between January 1 and September 28.

The baker is also effectively adapting its services to meet the needs of the modern consumer. Recent measures include introducing a click and collect service, building self-service outlets and extending opening hours into the evening.

Today, Greggs trades on a forward price-to-earnings ratio of 20.8 times. While the stock isn't cheap, I don't think this will hurt its chances of generating more impressive gains after last year's healthy rise.

{kind=link}