NEWSLETTER

NEWSLETTER

Image Source: Getty Images

The actions of the United Kingdom have been largely recovered since the bottom about two years ago. However, some have been left behind. One of those actions is Jet (LSE: Jet2).

While Jet2 increased by 137% for five years, this comparison begins from a very low base. On the other hand, we can see that the airline stock is flat instead of where it was in December 2020, for the context, the United Kingdom was locked at that time.

In other words, zero growth price growth in four and a half years. And that in itself is a danger. I like actions with impulse because they are more likely to reach the faster value.

However, this lack of impulse is a risk that I am willing to run with Jet2. Recently I have added it to my portfolio. I just think the stock is very undervalued.

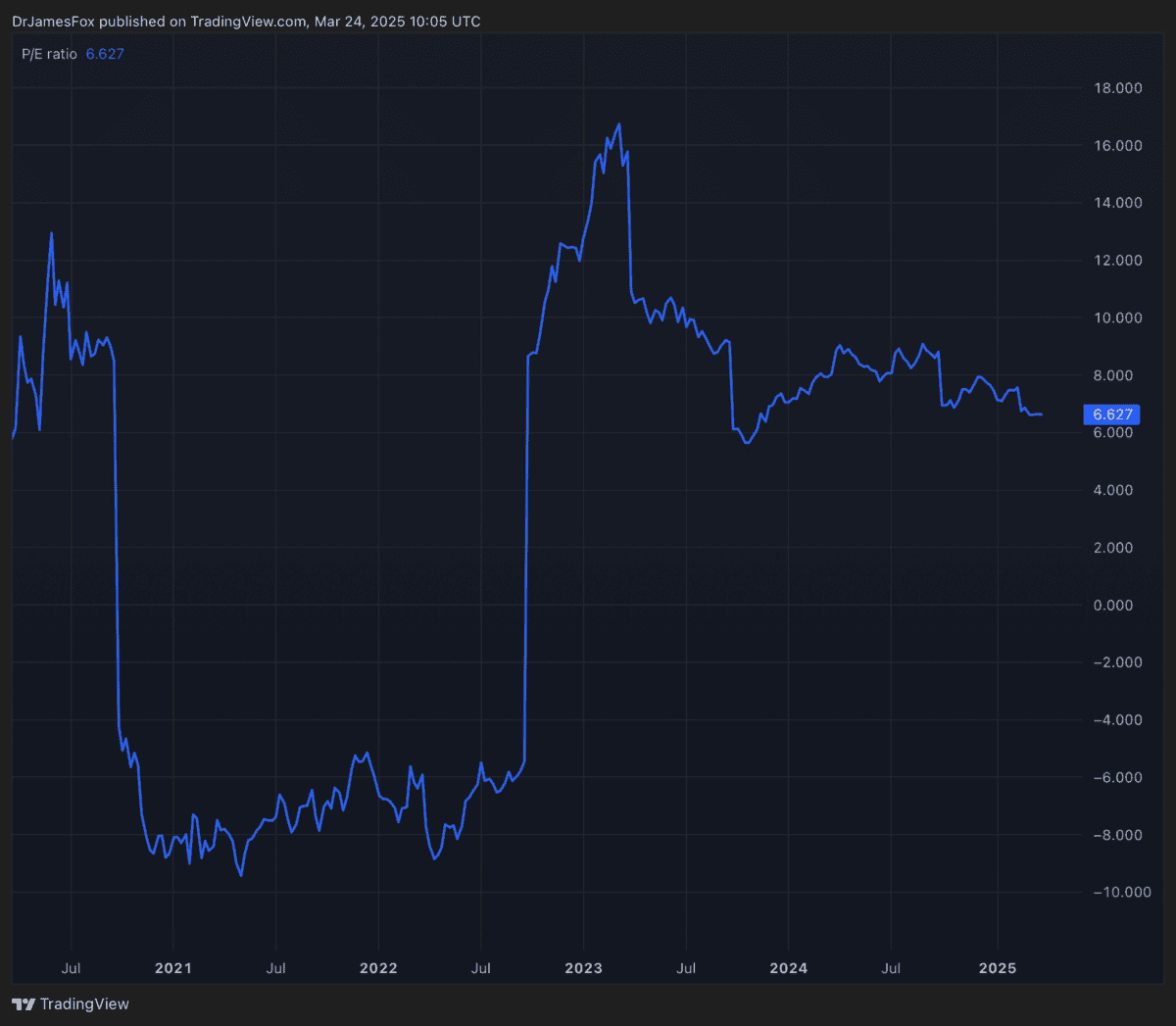

This is what the graphics say

Jet2 shares are quoted about seven times progress gains. That is not expensive for companies that quote in the United Kingdom and is not particularly expensive for airlines. The average of global airlines is currently around 7.4 times.

The above data shows that the ratio price ratio (p/e) fluctuates, but is back in line with where I was five years ago. We can also observe the impact of P/E on profits in 2020 and 2021, when it became negative.

However, the real indicator of value is the EV-EBITDA ratio. Most airlines do not have a net cash position, but Jet2 has £ 2.3 billion in net cash. As a result, its EV -bitda relationship is actually quite close to one. In other words, its business value is almost covered by only one year of Ebitda (profits before interest, taxes, depreciation and amortization).

Compared, IAG It officiates 5.4 times the term gains and with an avoidance ratio of 3.4. The inference here is that Jet2 has been greatly overlooked.

General description of a company

Jet2, the largest inclusive tourist operator in the United Kingdom and a leading leisure airline, is strategically positioned for growth despite facing industry's challenges. Analysts anticipate the growth of medium -term profits, backed by the presence of the expansion market of Jet2 and investments in the modernization of the fleet.

The Leeds -based company has a slightly older fleet, at 13.9 years, that some of its teammates. And Jet2 plans to invest £ 5.7 billion between 2025 and 2031 to improve its fleet, passing to a majority Airbus Configuration and increase capacity of 135 to 163 aircraft. The new A321neo plane is expected to improve operational efficiency with lower fuel consumption and greater seat capacity.

This investment is aligned with the industry standards, which represents approximately 11.4% of the projected income by 2025 and decreases even more as the income grows to an estimate of £ 8.6 billion by 2027. In fact, it is predicted that the company's net cash position reaches £ 2.7bn by 2027.

However, investors must write down potential risks. The increase in costs, including wages, airport charges and maintenance expenses, could press the profit margins. In addition, competitive prices in the European leisure market and a tendency towards subsequent reserves can create challenges.

Despite these challenges, the strong position of the Jet2 market, the cash position, the assessment and strategic investments are convincing. That is why I will continue looking to add to my position to current prices.

(Tagstotranslate) category. Category

{kind=link}