Image source: Getty Images

He S&P 500 jumped 23.3% last year, the second consecutive annual increase above 20%. And it will already be around 2% higher in 2025.

But is the rising index heading toward a correction (i.e., a 10% drop)? Here are my thoughts.

Arguments in favor

Incredibly, the S&P 500 has returned more than 20% in four of the last six years. In terms of total return (including dividends), it has been above 25% for four of those years, with a Covid-hit 2020 producing “only” 18.4%.

| Year | Price return | Total profitability |

|---|---|---|

| 2019 | 28.88% | 31.49% |

| 2020 | 16.26% | 18.40% |

| 2021 | 26.89% | 28.71% |

| 2022 | −19.44% | −18.11% |

| 2023 | 24.23% | 26.29% |

| 2024 | 23.31% | 25.02% |

However, historically these returns are much higher than typical for the index. In fact, the last period in which such monstrous returns occurred clustered was the late 1990s. And we know what followed that boom…

| Year | Price return | Total profitability |

|---|---|---|

| 1995 | 34.11% | 37.58% |

| 1996 | 20.26% | 22.96% |

| 1997 | 31.01% | 33.36% |

| 1998 | 26.67% | 28.58% |

| 1999 | 19.53% | 21.04% |

| 2000 | −10.14% | −9.10% |

| 2001 | −13.04% | −11.89% |

| 2002 | −23.37% | −22.10% |

Of course, this does not guarantee that something similar will happen this time. But then as now, a revolutionary new technology emerged that was exciting investors (the Internet and artificial intelligence (ai), respectively). Could history rhyme here? It is possible.

Additionally, Donald Trump has promised or threatened widespread tariffs, which many economists predict will be inflationary. If so, this would be an obstacle to interest rate cuts.

Finally, the index is highly valued, with a forward price-to-earnings (P/E) ratio of 21.6. This high starting point makes it more difficult for corporate earnings to grow at a rate that justifies the valuation.

The index performed very strongly the last time Trump was in charge of the US economy. However, the multiple is currently around 27% higher than when he took office in early 2017. Therefore, a correction could be on the table.

Arguments against

Yesterday (January 20), the new President was sworn in. In his speech, he promised to increase consumers' purchasing power by reducing energy bills, taxes and inflation, thus strengthening the economy in the process. He even mentioned putting the American flag on Mars.

Given this optimism, one could argue that 2025 will be another positive year for the S&P 5OO. Rumors of a U.S. recession have faded, animal sentiment is strong, and interest rates still appear poised to fall.

How am I responding?

The mood in America right now is incredibly optimistic. My hunch then is that the index will rise this year, but it won't deliver a third consecutive double-digit return. Naturally, I could be totally wrong.

However, what I am most certain of is that specific stocks in the S&P 500 appear wildly overvalued. one is Palantir Technologies (NASDAQ: PLTR), whose stock price has soared 1,017% since the beginning of 2023.

Palantir offers artificial intelligence solutions to both government organizations and enterprises. It's been growing like wildfire, with third-quarter revenue up 30% year-over-year to $725 million.

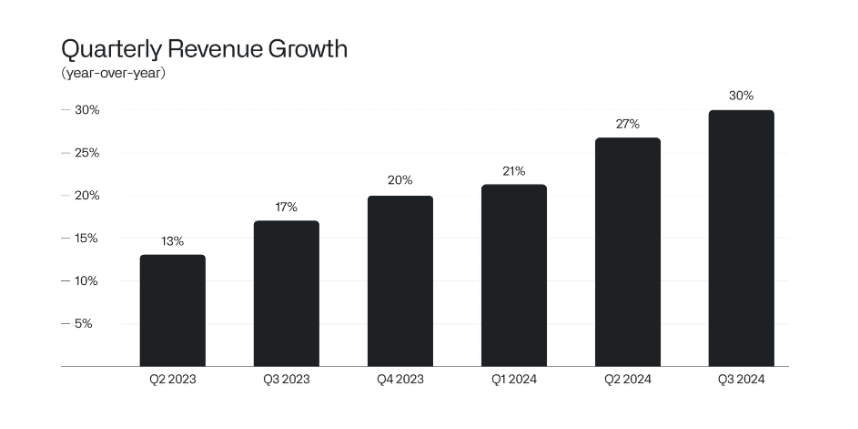

In fact, revenue has accelerated for six consecutive quarters!

Palantir also generated a record net profit of $144 million. And CEO Alex Karp struck an incredibly optimistic tone: “A giant is emerging. This is the century of software and we intend to conquer the entire market..”

So, it's clear that there are a lot of things to like about this ai company. However, the stock is trading at an incredible price-to-sales (P/S) multiple of 66. The forward P/E ratio is above 150. If growth normalizes, these valuations are likely unsustainable.

Palantir is the kind of overvalued S&P 500 stock I'm avoiding right now.

{kind=link}