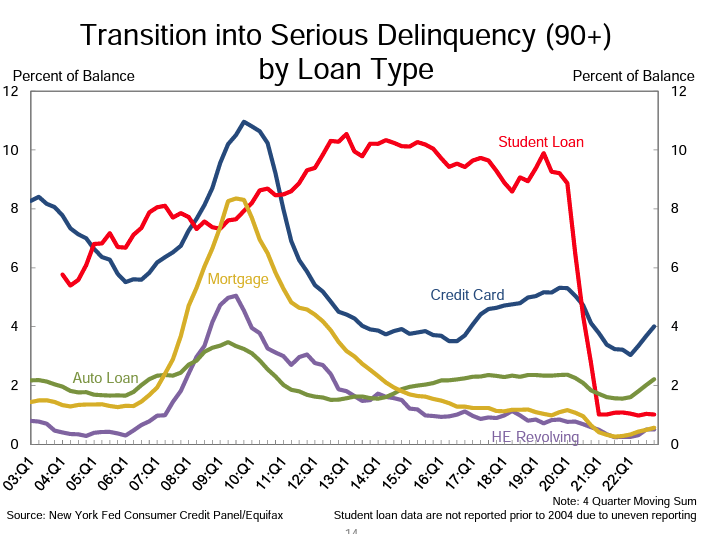

spxChrome/iStock via Getty Images

Credit card metrics for January generally show some deterioration in credit quality as consumers come to grips with the reality of their vacation spending. That means that the data for the month is often skewed by seasonal trends. Taking the bigger picture, yeah, credit The quality is trending down as the pandemic-era stimulus programs are long overdue (except for the pause in federal student loan payments).

Baird analyst David George, who covers six of the seven stocks in the table below, summarized credit card metrics for January and said net charge-offs were worse than typical seasonality, the pay-off rate for Seasonal lending was higher than expected and delinquencies increased M/M in line with seasonal expectations. The only stock George does not cover on the Seeking Alpha chart is Bread Financial (New York Stock Exchange: BFH).

In the bigger picture, card losses continue to approach the “normal” range, that is, the pre-pandemic level, which he expects to occur during fiscal year 2023, George said. His recommendation on his stock is to wait until American Express (New York Stock Exchange:AXP) and Capital One (NYSE:COF) goes back before adding positions.

Discover Financial (New York Stock Exchange: DFS) saw its January delinquency rate of 2.67% hit the pre-pandemic level of 2.65%; its 2.81% net churn rate is still well below the 3.45% in January 2020.

Wolfe Research analyst Bill Carcache notes that Discover (DFS) and Bread Financial (BFH) exceeded their 2019 levels. For the five credit card stocks he covers (AXP, COF, DFS, SYF, and BFH), the Delinquency rates increased on average 99 basis points Y/Y and remain 44 bp below 2019.

It reiterates its underweight stance on card issuers as Wolfe Research macro strategist Chris Senyek believes the Federal Reserve will trigger a recession as it tries to cool labor markets.

“We expect delinquency rate formations to continue to rise in the coming months before accelerating later in the year as long and variable lags associated with monetary policy” will eventually fuel an increase in initial jobless claims, it said. Carcache in a recent note. As a result, he expects a “modest downgrade in credit and higher net write-offs (30% above 2019 levels, helped by denominator effects as loan growth finally slows).”

| 2023 | 2022 | 2020 | ||||||

| Company | Heart | Guy | January | December | November | 3 month average | January | change in bps |

| capital one | COF | delinquency | 3.65% | 3.43% | 3.32% | 3.47% | 4.10% | -Four. Five |

| cancellation | 3.81% | 3.57% | 3.14% | 3.51% | 4.31% | -fifty | ||

| amexpress | AXP | delinquency | 1.00% | 1.00% | 0.90% | 0.97% | 1.60% | -60 |

| cancellation | 1.50% | 1.20% | 1.00% | 1.23% | 2.30% | -80 | ||

| JPMorgan | New York Stock Exchange: JPM | delinquency | 0.83% | 0.76% | 0.73% | 0.77% | 1.14% | -31 |

| cancellation | 1.17% | 1.24% | 1.64% | 1.35% | 2.19% | -102 | ||

| Synchrony | New York Stock Exchange:SYF | delinquency | 3.80% | 3.70% | 3.60% | 3.70% | 4.50% | -70 |

| adjusted cancellation | 4.30% | 3.40% | 3.70% | 3.80% | 5.20% | -90 | ||

| Discover | SFD | delinquency | 2.67% | 2.53% | 2.36% | 2.00% | 2.65% | 2 |

| cancellation | 2.81% | 2.54% | 2.46% | 2.60% | 3.45% | -64 | ||

| financial bread | BFH | delinquency | 5.80% | 5.50% | 5.40% | 5.57% | 6.00% | -twenty |

| cancellation | 6.70% | 6.70% | 6.10% | 6.50% | 7.20% | -fifty | ||

| Citigroup | New York Stock Exchange:C | delinquency | 1.04% | 1.01% | 0.98% | 1.01% | 1.58% | -54 |

| cancellation | 1.50% | 1.34% | 1.33% | 1.39% | 2.49% | -99 | ||

| Bank of America | New York Stock Exchange: BAC | delinquency | 1.09% | 1.03% | 1.02% | 1.05% | 1.61% | -52 |

| cancellation | 1.50% | 1.43% | 1.33% | 1.42% | 2.54% | -104 | ||

| average crime | 2.49% | 2.35% | 2.29% | 2.37% | 2.90% | -41 | ||

| average cancellation | 2.91% | 2.68% | 2.59% | 2.73% | 3.71% | -80 | ||

The Federal Reserve Bank of New York’s fourth-quarter household debt and credit report showed credit card balances hit a new high of $986 billion. That spells trouble when the next recession hits. “It’s a triple problem for credit card borrowers. Balances are up, rates are up, and more people are in credit card debt (46 percent of credit card holders, up from 39 percent a year ago). year),” said Ted Rossman, senior industry analyst at Bankrate. .

SA contributor Lance Roberts explains why the consumer is likely to be the biggest loser when the recession hits.

{kind=link}