NEWSLETTER

NEWSLETTER

Image source: Getty Images

Savings levels in the UK have reached record levels of over £2bn in 2024. But could prioritizing savings over buying UK shares be costing people a lot of money?

I think so. And new research from Janus Henderson Investment Trusts supports that view. It shows that cash savings “returned less than a third of what was returned from stocks and shares”in the nine months to September.

It means Brits have literally missed out on tens of billions of pounds.

A black hole worth £165bn

According to Janus Henderson, savers earned £58.6bn in interest between January and September, equivalent to an average interest rate of 2.93%.

In comparison, the FTSE All-Share Index It earned a 9.9% return through a combination of capital gains and dividend income. Meanwhile, the MSCI World Index provided an even higher return of 13.4%.

The result in real terms is astonishing. Using the calculations of Janus Henderson, “Savers have missed out on £165bn in returns… when comparing cash interest and global share returns..”

The report adds that “Savers have lost £110 billion in returns this year compared to investing in UK shares..” Both calculations even allow you to keep your household income for three months in a savings account.

Long term trend

This striking difference is not just a temporary development, either. And it's even more depressing for cash savers when we take into account the eroding impact of inflation.

Janus Henderson says that “£100 saved in cash have lagged behind price increases by 3.4% over the past 30 years, meaning they buy less today, even with all the interest income earned since then, than they did in 1994..”

By contrast, that £100 invested in global shares would have outpaced inflation almost seven times, or four times if it had been spent on UK shares.

A superior background

Past performance is no guarantee of future success. But the resilience and wealth-creating power of the stock market is the reason most of my money is tied up in stocks, funds and trusts.

I just have some money in a savings account to manage risk and give myself cash to use in case of a rainy day. While this is a riskier strategy, I can take steps to reduce the danger by diversifying my holdings.

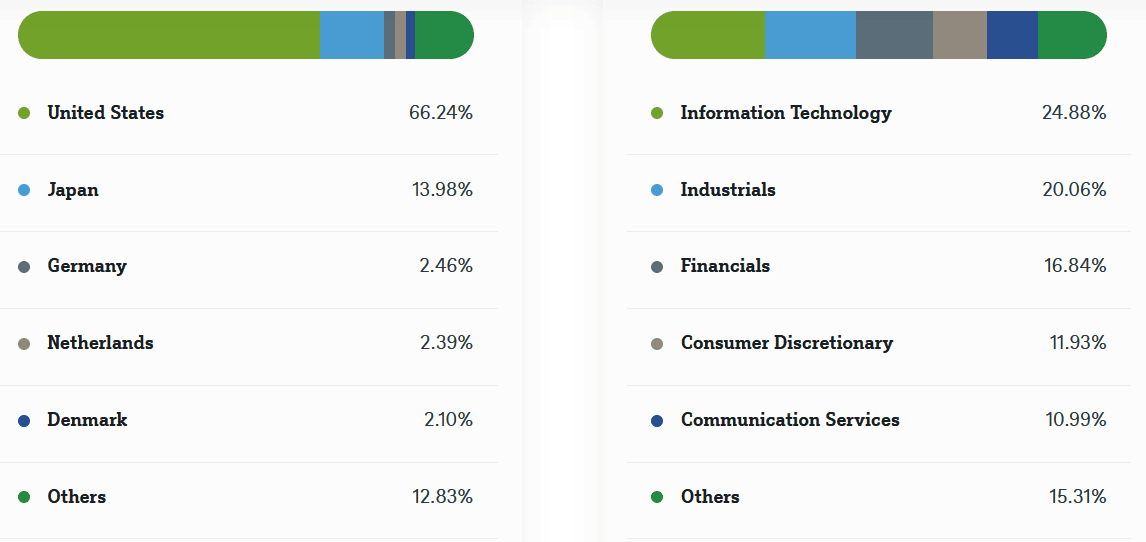

One strategy I use is to invest part of my capital in exchange-traded funds (ETFs) such as Xtrackers MSCI World Momentum UCITS ETF (LSE:XDEM).

As its name suggests, this fund invests in stocks from all over the world, 350 in total. And so it allows me to spread risk across a variety of regions (including the UK) as well as a multitude of sectors.

I like the decent exposure to tech stocks, including NVIDIA, Apple and Goal. This gives me the opportunity to capitalize on rapidly growing technological phenomena such as artificial intelligence (ai), robotics and quantum computing. But I'm aware that stocks like this could offer disappointing returns during economic downturns.

Since 2014, this fund has achieved an average annual return of 11.9%. If this continues, an investment of £10,000 today would become £348,975 after 30 years.

That's much better than the £24,568 you could have earned by depositing £10,000 into a savings account yielding 3%.

stocks and funds can go up and down in price. But results like this suggest that my current strategy is the right one for me.

{kind=link}