NEWSLETTER

NEWSLETTER

Much has been said about Ethereum trading Bitcoin in the past, particularly during the 2017 bull cycle when the ETH/BTC ratio peaked at 0.157.

However, fast forwarding to now, spurred on by the ongoing banking crisis narrative, Glassnode data analyzed by CryptoSlate suggests a period of Ethereum underperformance ahead, putting an end to the idea of a “turnaround”.

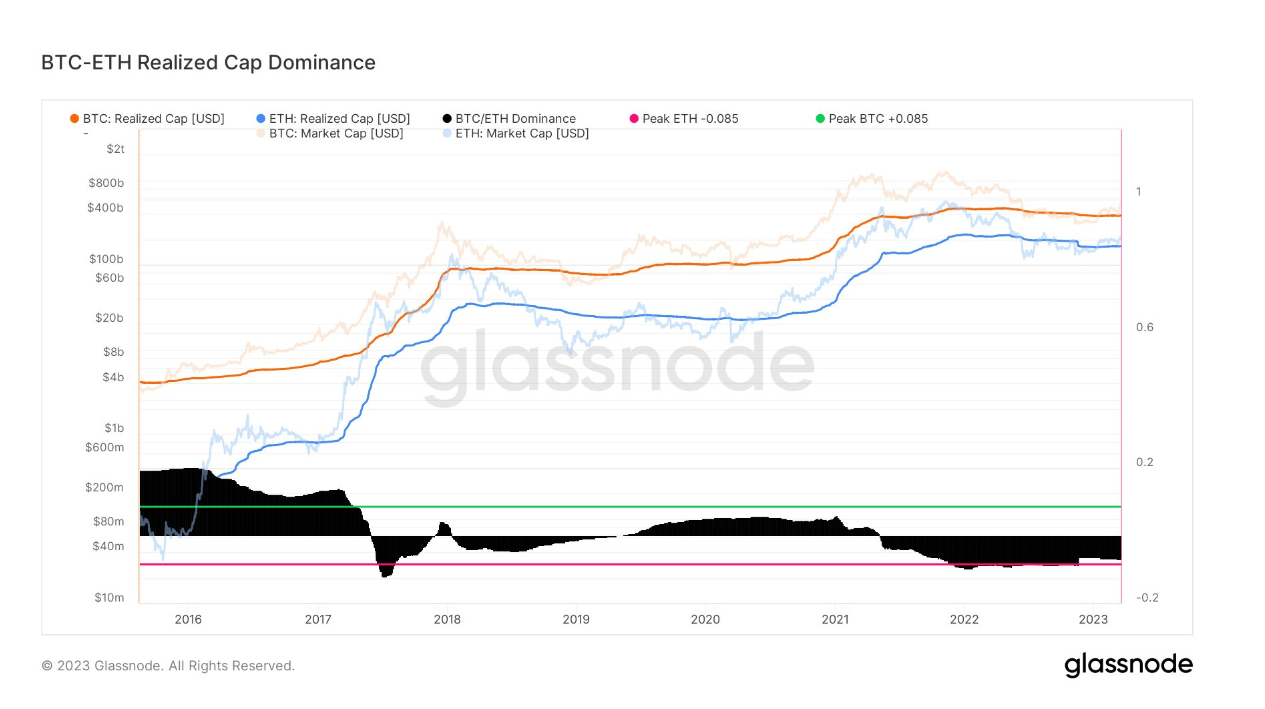

Bitcoin – Ethereum Realized Cap Dominance

Market capitalization is the most popular way to value and compare cryptocurrencies. It is calculated by multiplying the current price by the current supply.

A variation of the market capitalization method is realized capitalization, which replaces the current price in the previous calculation with the price when the coins last moved. Proponents argue that this gives a more accurate valuation because it minimizes the effects of lost and unrecoverable coins.

The chart below documents the Bitcoin and Ethereum market and realized caps since 2016. It shows a tightening between BTC and ETH in June 2017, especially when looking at the realized cap lines.

Around April 2019, the two began to diverge. But by May 2021, a further tightening of the two gangs took place. However, Ethereum’s realized cap has started to decline in recent weeks, and Bitcoin is holding relatively steady.

The chart also plots BTC/ETH dominance, calculated by taking the BTC market cap and dividing it by ((BTC market cap + ETH market cap) – 0.765). The 0.765 figure visualizes the oscillator around a long-term mid-value. It shows that the market is starting to emerge from a two-year period of ETH dominance.

Based on the current situation, markets are preparing for higher rates and banks continue to restrict the availability of credit, a generally favorable scenario for risky assets.

Ethereum is considered a riskier and higher beta than Bitcoin, suggesting that it will underperform the leading cryptocurrency entering a risk averse environment.

Ethereum Fundamentals

Analysis of Ethereum’s fundamentals also suggests underperformance going forward.

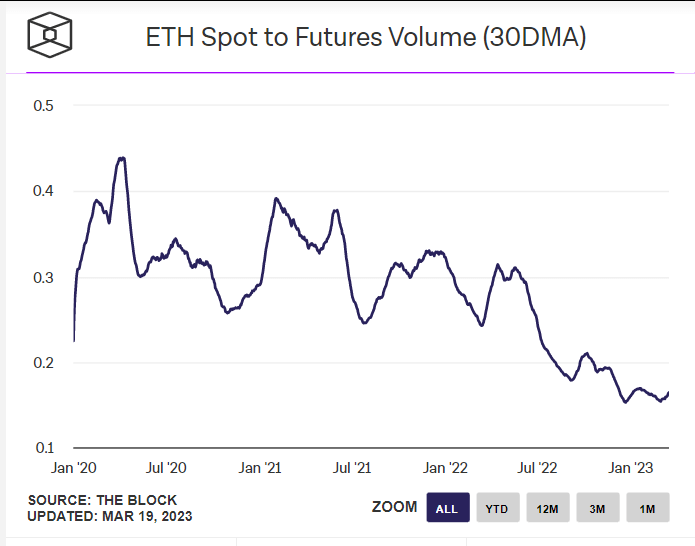

A general indicator of ecosystem health is a high/increasing Spot to Futures ratio: this indicates an ecosystem where holders dominate traders, whose intent is to make a profit rather than believe in the ecosystem.

The Block on ETH Spot to Futures volume data shows a macro downtrend since April 2020. The downtrend accelerated around May 2022 (Terra-LUNA implosion) and has since fallen to an all-time low.

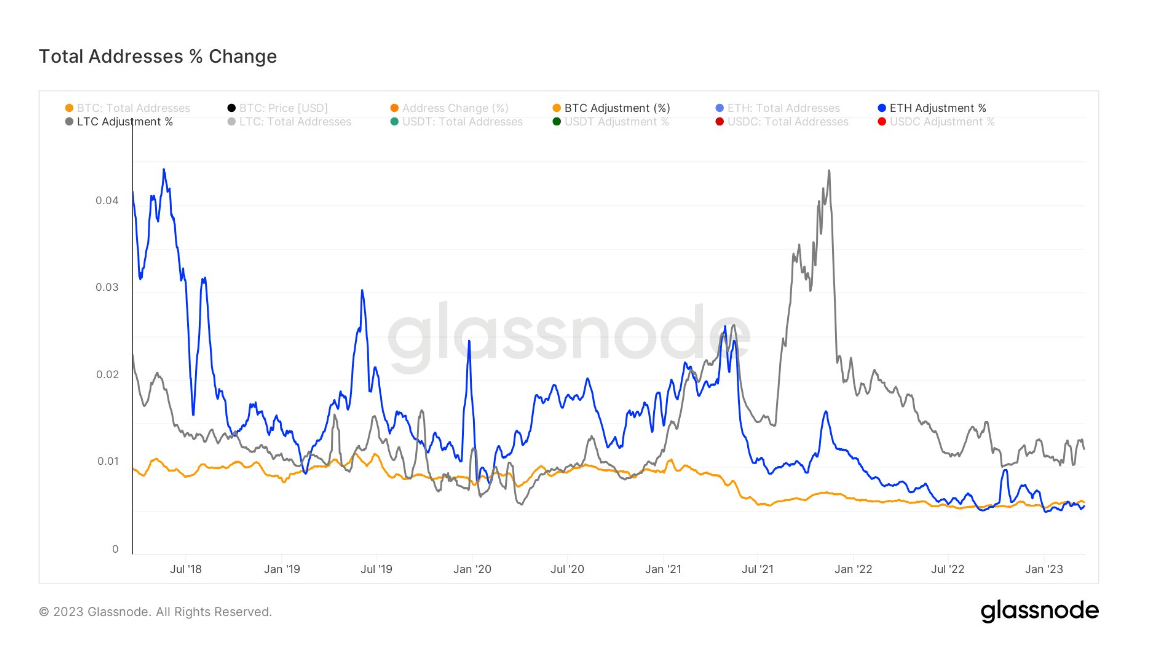

The percentage change in total ETH addresses has been declining over the past five years, falling below BTC last month.

Similarly, the percentage change in total LTC addresses started to move away from ETH (and BTC) around June 2021, staying consistently higher ever since, particularly moving towards the top of the market around November 2021.

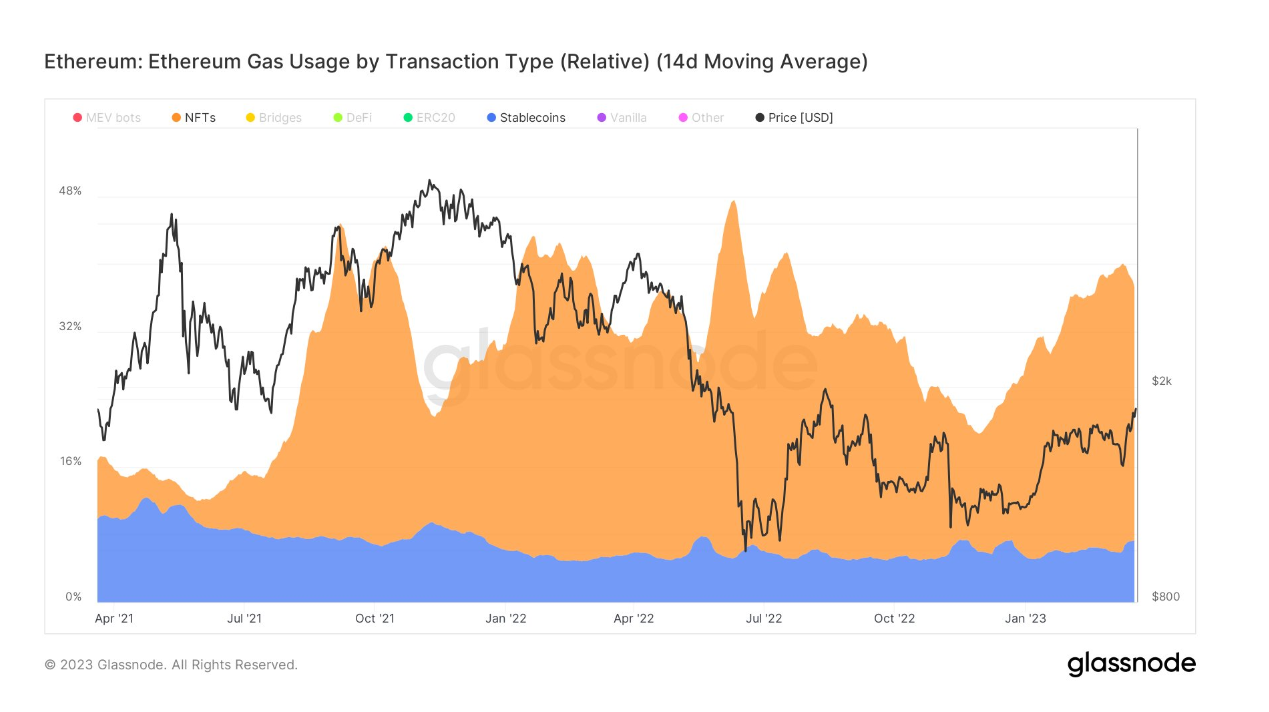

On-chain data shows that stablecoin and NFT transactions make up the most significant gas use in ETH, with the former rising around December 2022. The latter have been flat, relatively flat since April 2021.

In June 2022, stablecoin and NFT transactions accounted for almost half of ETH gas usage. Now, the percentage is around 35%, indicating a general drop in these applications on the ETH chain.

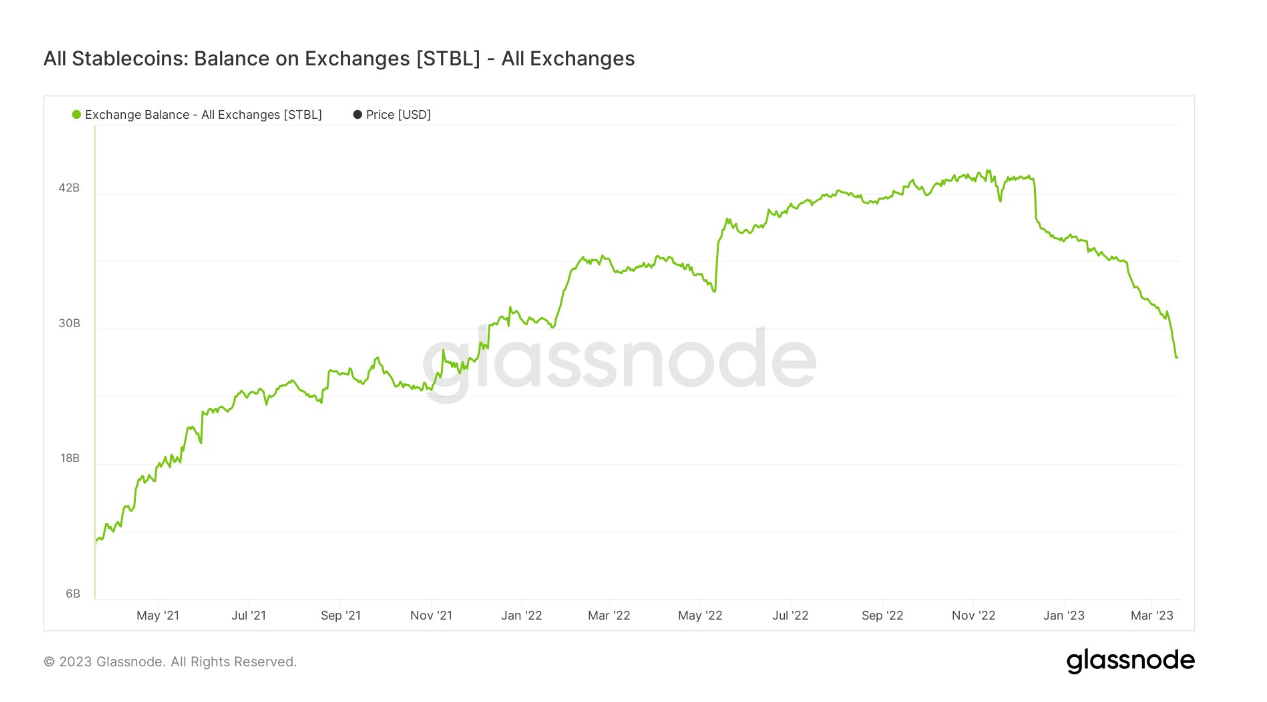

This can be explained by the growing popularity of ordinals in BTC, which has somewhat decreased the demand for ETH NFT. Similarly, stablecoins on exchanges have sunk to a 17-month low, suggesting an overall decline in their importance to cryptocurrencies, likely due to ongoing narratives about their safety/redeemability.

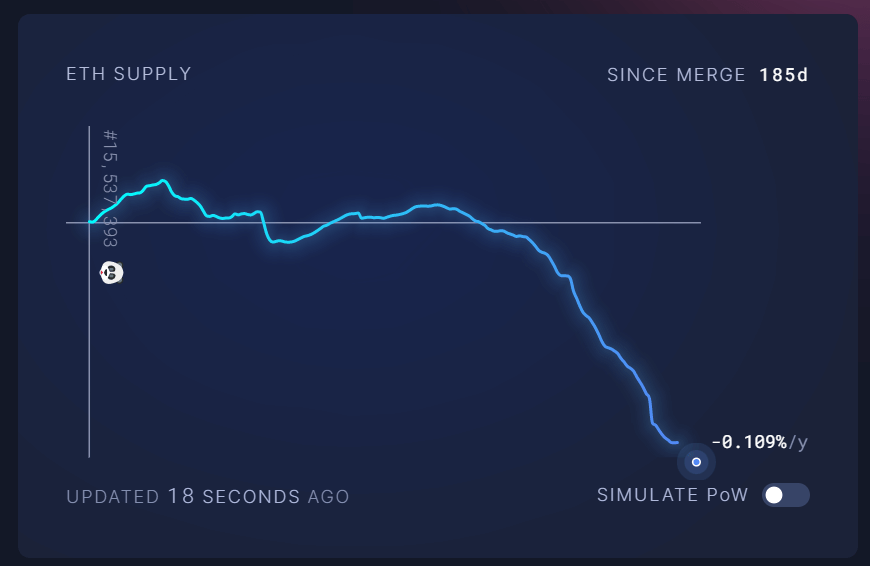

The Merge narrative led to bullish price drivers in the switch to proof-of-stake and deflationary tokenomics. However, more than six months later, ETH is still losing against Bitcoin. Several reasons could be behind this.

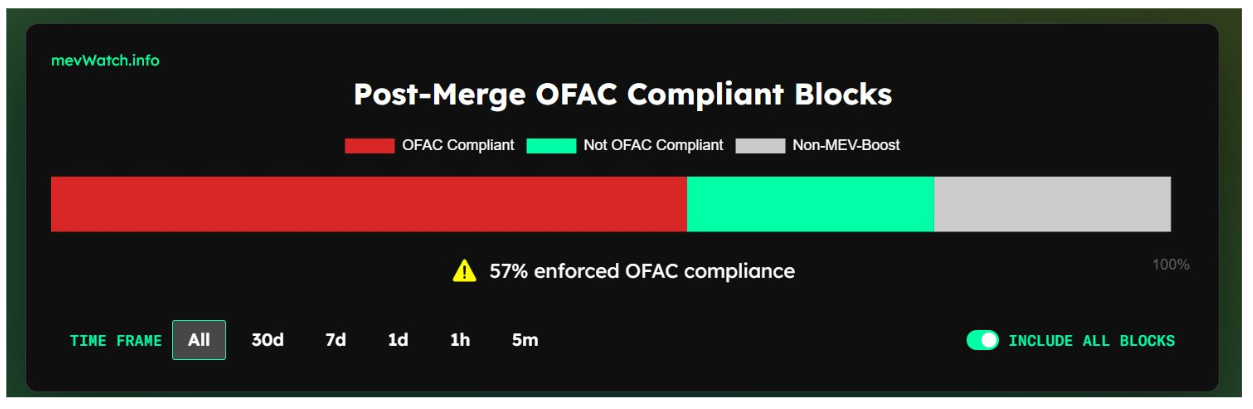

Since the Tornado Cash sanctions, Ethereum’s reputation as a decentralized and uncensorable chain has taken a significant hit. More than half of the blocks are still Office of Foreign Assets Control (OFAC) compliant, which means that more than half of the network will exclude transactions at the behest of US authorities.

Additionally, while the developers were transparent in stating that the merger would not directly reduce fees, there remains an unresolved issue with expensive transactions. The chart below shows that transaction fees recently skyrocketed to roughly 5k ETH.

The ETH/BTC ratio is currently at 0.0635, less than half what it was during the 2017 peak. There has been a notable drop in the ratio since the banking crisis, suggesting that the market overwhelmingly favors Bitcoin these days. uncertain times.

{kind=link}