NEWSLETTER

NEWSLETTER

Shanghai is the next major Ethereum upgrade, scheduled to go live on April 12th.

Once implemented, the ETH staked in the staking contract will be unlocked and withdrawable, thus completing the process that began with the launch of the Beacon Chain in December 2020.

The implication of the Shanghai update is subject to much speculation. Some expect the spot price to stagnate as holders sell off. Others believe that getting in and out of the participation contract will easily attract more takers, leading to price stability.

Glassnode data analyzed by CryptoSlate Ethereum derivatives traders suggested that they are cautious going into the Shanghai update. However, after Shanghai, sentiment eases.

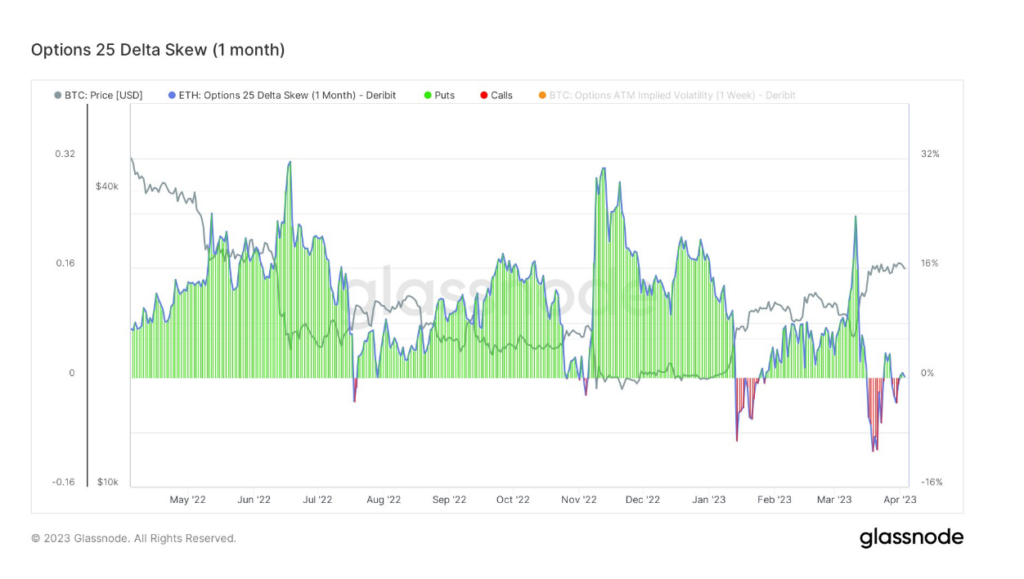

Ethereum – 25 Delta Skew Options

The Options 25 Delta Skew metric analyzes the proportion of put-to-call options expressed in terms of implied volatility (IV).

A call option gives the holder the right to buy an asset, and a put option gives the holder the right to sell an asset.

For options with a specific expiration date, this metric analyzes put options with a delta of -25% and call options with a delta of +25%, offset to arrive at a data point, giving a measure of the sensitivity of the option price taking into account the change in the spot price of Ethereum.

Typically, this metric can be organized by periods in which the option contract expires, such as one week, one month, three months, and six months.

The chart below relates to options expiring in one week (near term); shows that put options are now at a premium, suggesting the market is cautious as the Shanghai launch approaches.

The 1-month Delta Skew at 25 is somewhat balanced between puts and calls, pointing to a settling in sentiment post-Shanghai.

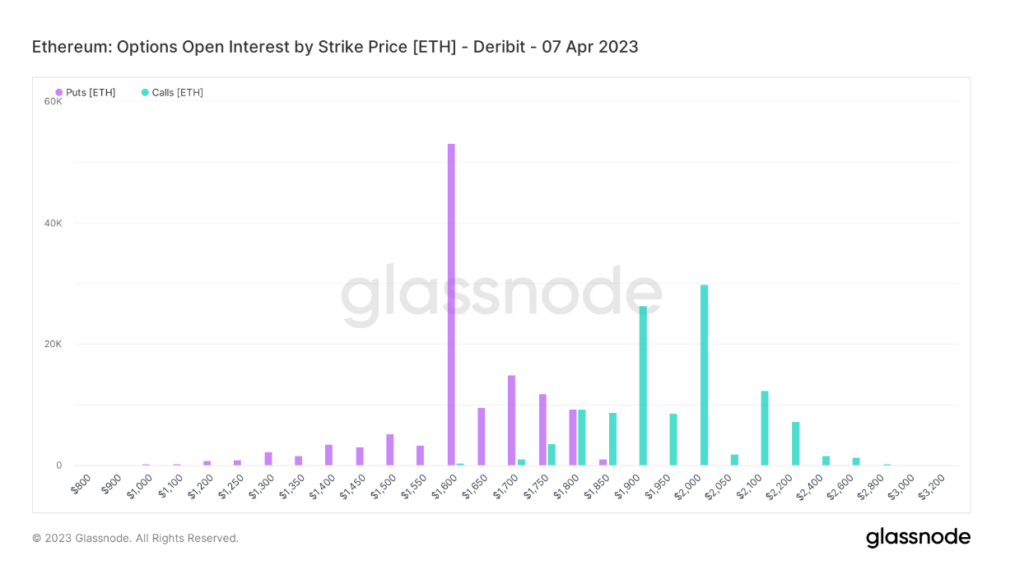

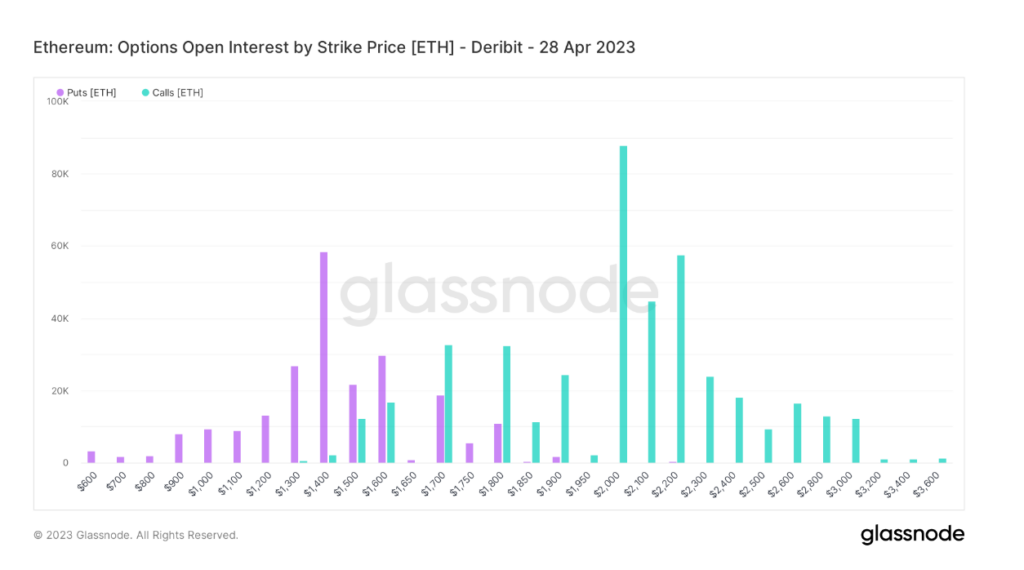

open interest

The open interest by exercise price refers to the total number of derivative contracts pending settlement, organized by the exercised sale or purchase price.

This metric is used to measure general market sentiment, particularly the force behind buy or sell price trends.

The chart below for April 7 shows put options dominating, with the $1,600 strike price well ahead. in more than 50,000 contracts.

Looking beyond the Shanghai launch date, toward the end of April, the frequency of calls vs. calls has evened out compared to April 7. However, sentiment turns the other way, with $2,000 call options being the most prevalent option at around 90,000 contracts.

As such, moving into the next month, traders are signaling a more bullish outlook.

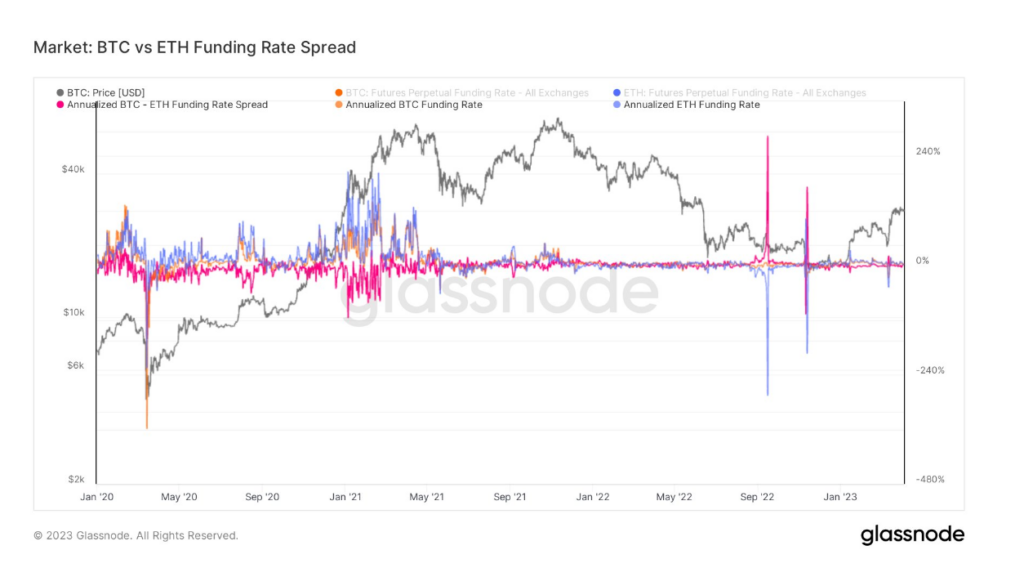

Funding Rate Margin

The financing rate refers to periodic payments made to or by derivatives dealers, both long and short, based on the difference between the perpetual contract markets and the spot price.

When the funding rate is positive, the price of the perpetual contract is higher than the marked price. In such cases, long traders pay short positions. Conversely, a negative funding rate shows that perpetual contracts are priced below the marked price, and short traders pay for longs.

This mechanism ensures that futures contract prices fall in line with the underlying spot price.

In this case, the spread refers to the difference in the annualized funding rates of BTC and ETH.

During the merger in September 2022, ETH’s annualized funding rate fell to -282%, indicating that short traders were overwhelmingly bearish and willing to pay for longs.

Fast forward to now, the magnitude of the moves has been reduced significantly compared to last September. Yesterday, ETH traders posted a slightly positive funding rate of 0.14%, suggesting slightly bullish sentiment. Compared to the BTC funding rate of 2.8%, this indicates a slightly more pessimistic view than Bitcoin traders.

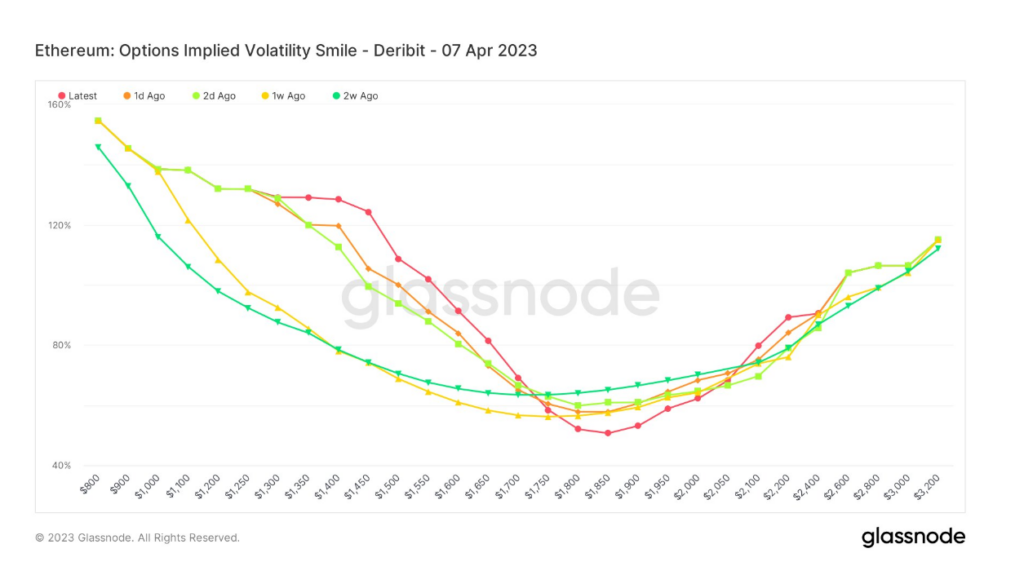

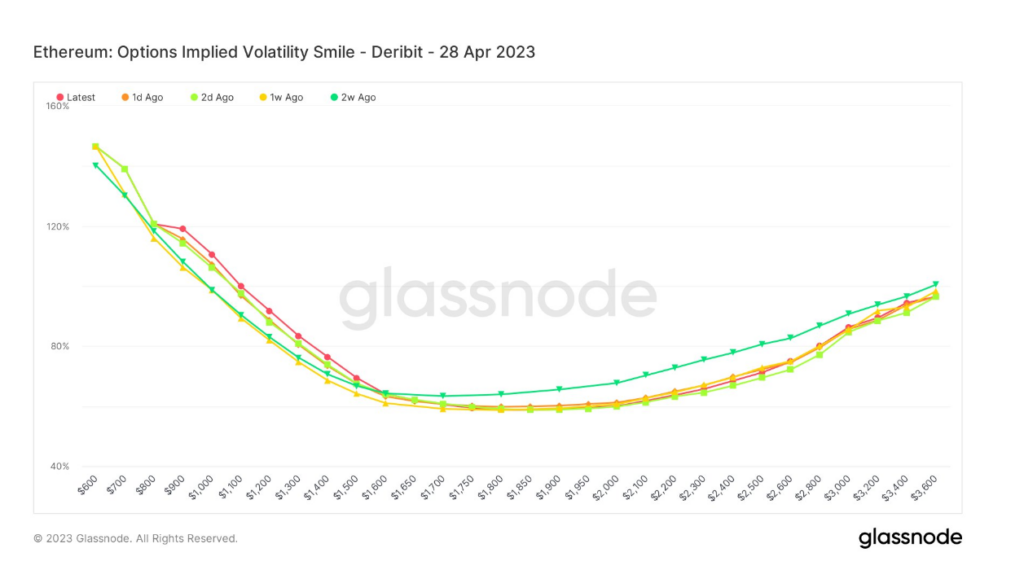

Implied Volatility Smile

The volatility smile results from plotting the strike price and implied volatility (IV) of options with the same underlying asset and expiration date.

The IV increases when an option’s underlying asset is more out-of-the-money (OTM), or in-the-money (ITM), compared to at-the-money (ATM).

More OTM options generally indicate higher IVs, giving Volatility Smile charts their distinctive “smile” shape. The tilt and shape of the smile can be used to assess the relative cost of options and measure what kind of tail risks the market has included.

By comparing the “Last” smile to the historical overlays of one day, two days, one week, and two weeks ago, it is possible to determine the degree of implied volatility on each side of ATM.

The chart below shows that markets are paying a premium for downside protection ahead of the Shanghai update. IV is well above 100%.

After the upgrade, markets continue to pay a premium for fall protection. But the patterns have smoothed out significantly, showing a slight taper on the right tail, with a relatively flat shape and IV less than 100% on the right side curve.

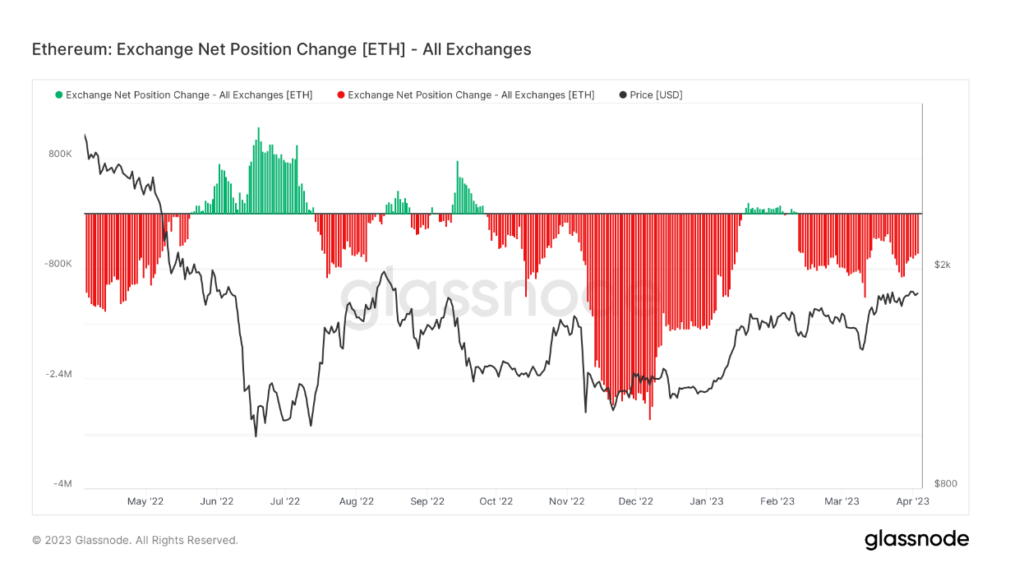

punctual demand

Exchange Net Position Change (ENPC) measures coins deposited or withdrawn from exchange wallets.

Entries or positive change are generally considered bearish, since the main reason to transfer to an exchange is to sell. While outflows, or negative change, are generally considered bullish, the main reason for pulling out relates to wallet storage, hence retention.

Since mid-February, ETH’s ENPC has turned negative, suggesting strong demand for spot in the run-up to Shanghai.

The post Investigation: Ethereum Derivatives Traders Signal Caution Before Shanghai Update first appeared on CryptoSlate.

{kind=link}