Image source: Getty Images

It's always a little surreal when a company in your stocks and Shares ISA starts trending around the world. That's what happened to me recently with a cybersecurity company. Mass coup (NASDAQ: CRWD).

This is the kind of company I want operating behind the scenes, protecting its customers from cyber threats with its cloud-native Falcon platform. If its name is suddenly on everyone’s lips, then I assume a massive cyberattack has occurred.

However, as we know, that's not what happened a few days ago. A faulty software update bricked 8.5 million devices. Microsoft Windows computers shut down, causing disruptions to flights, banks, television stations and hospitals around the world. It was the largest IT outage in history.

Following this, CrowdStrike's stock price dropped by 23%. Is this an opportunity to buy more shares?

A household name (for the wrong reason)

The first thing to keep in mind is that there will obviously be significant complaints about this epic failure. Delta airlinesFor example, it has had to cancel more than 4,000 flights.

This event even caused volatility among the largest cyber underwriters in the primary and reinsurance markets. Barclays saying: “At present, due to the short duration of the accident and its non-malicious nature, we would expect (sure) Industry impact of $1 billion or less.”

As disturbing as this was, and certainly embarrassing for CrowdStrike, a large-scale cyberattack would have been worse, destroying confidence in the company's defensive capabilities.

On the other hand, there is still the reputational damage, which cannot be quantified and will take time to measure.

What we do know is that Elon Musk has said that Tesla It has already removed CrowdStrike from its systems. It is possible that others will follow suit and that would obviously affect the company's growth prospects.

An important platform

Step back, however, and the widespread impact of this event highlights just how important the company’s endpoint security platform has become. It now serves 538 of the Fortune 1000, while its artificial intelligence (ai) technology is getting smarter as it consumes more data.

Between FY19 and FY24 (ending in January), revenue grew more than 10-fold.

In the first quarter of fiscal 2025, the company generated record free cash flow of $322 million, up from $227 million a year earlier. That represented 35% of its $921 million in revenue, which grew 33%.

It has been rolling out more ai features, with 28% of its customers adopting seven or more of its 28 cloud modules, up from 23% a year earlier.

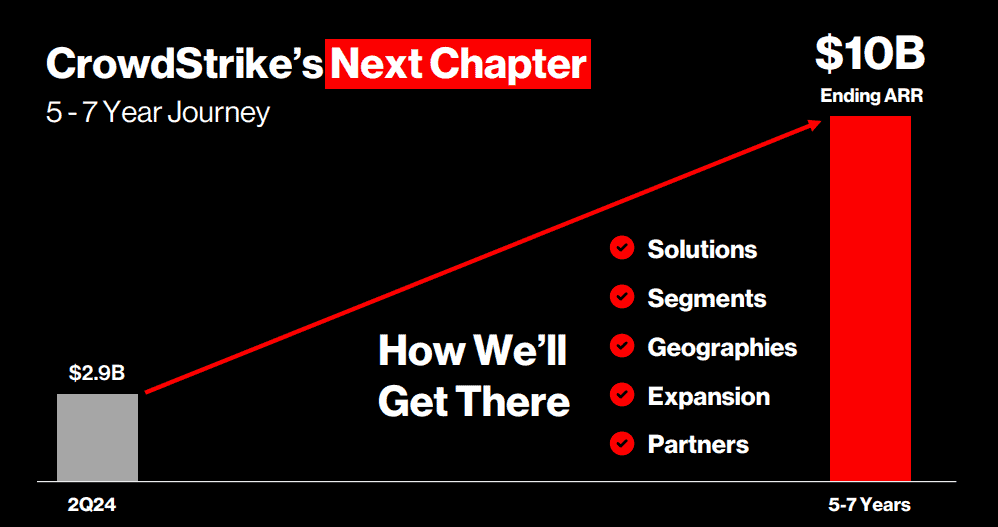

Looking ahead, the company aims to achieve $10 billion in annual recurring revenue (ARR) over the next five to seven years. At the end of the first quarter, ARR stood at $3.65 billion.

Of course, this goal was achieved before the software update debacle.

My movement

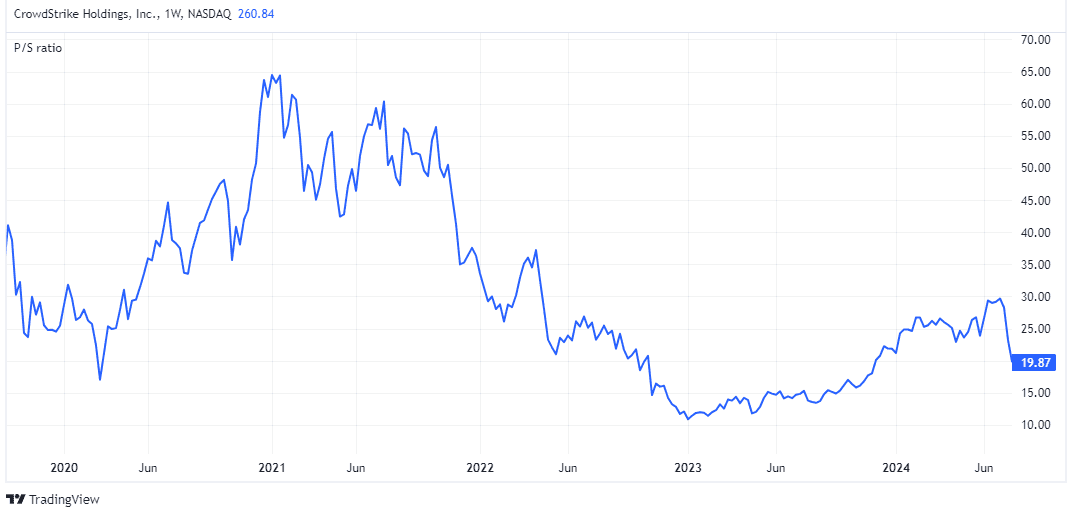

CrowdStrike is trading at around 20 times its sales, even after the 23% drop. So it is still a very expensive stock, priced perfectly.

Things aren't perfect, though. Growth rates could fall if problems arise with renewals and attracting new customers. In the meantime, the company might have to offer some price concessions or redesign the way its software interacts with devices, which would put pressure on profitability in the short term.

However, it remains one of the best cybersecurity stocks in its category. If it continues to fall, I will consider investing more money, but I would prefer to wait until the second quarter of August to hear management speak.

{kind=link}