Image source: Getty Images

Legal and general (LSE:LGEN) shares currently have a dividend yield of 9.3%. That is higher than the FTSE 100 average, well above inflation and much better than the interest available on cash.

That makes it seem like investors looking for passive income should invest in stocks. If it were that easy, the reality is (unfortunately) a little more complicated.

Five-year returns

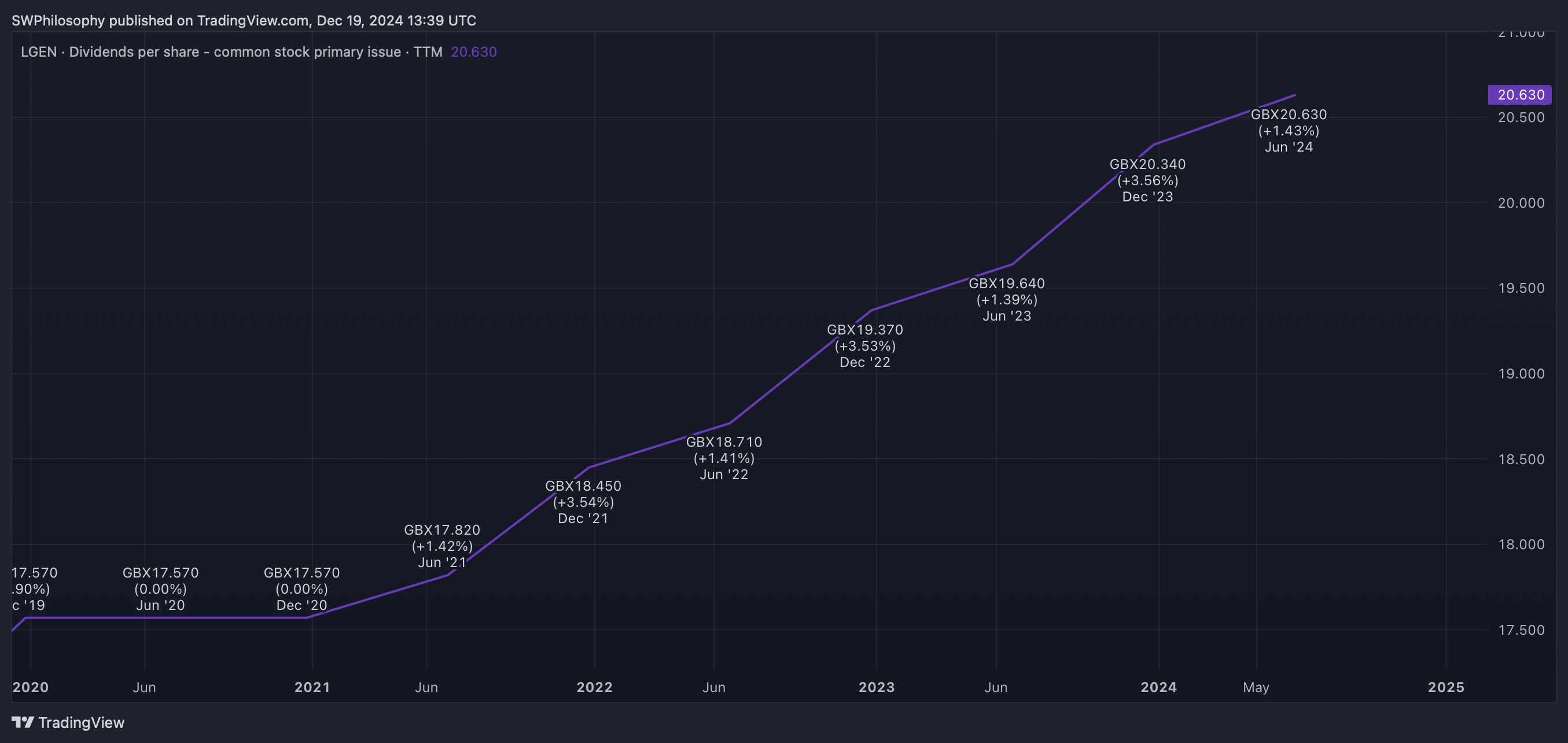

Five years ago, Legal & General was trading with a dividend yield of 6.6%. Things were different back then, but it was still a striking comeback.

Since then, the company has increased its distributions to shareholders each year. The average annual increase has only been about 3%, but it has been impressively consistent.

Statutory and general dividends per share 2020-24

Created in TradingView

The problem is that this has not translated into a great result for shareholders. While it paid a total of 94.37p per share, this was largely offset by the share price falling 82.44p in that time.

As a result, investors who bought shares in December 2020 returned a total of 3.9% on their investment. That's lower than the FTSE 100, well below inflation and even worse than the return available on cash.

Is the dividend safe?

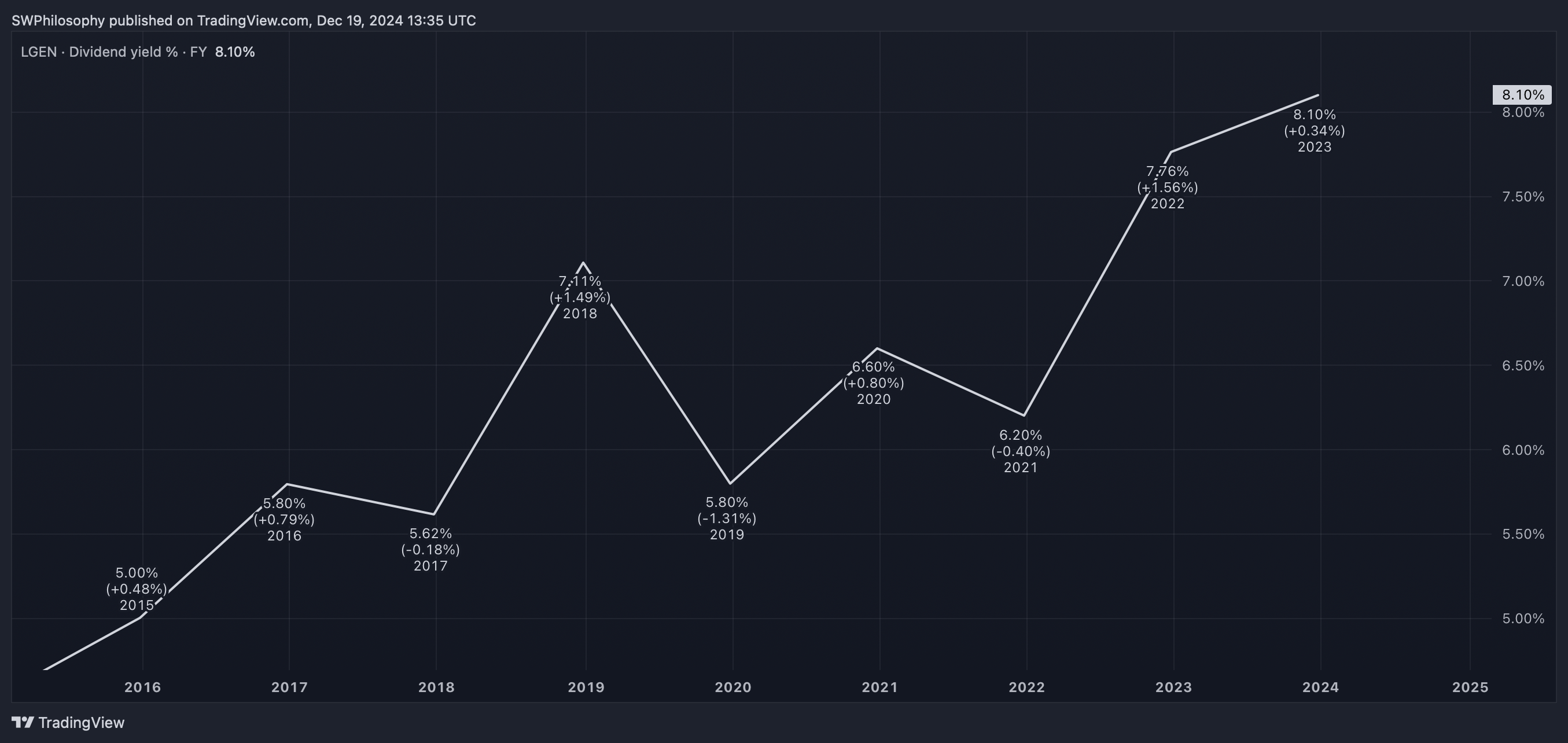

A dividend of 9.3% offers much more protection against a share price decline than one of 6.6%. And performance has not been at this level at any time in the last 10 years.

Legal and general dividend yield 2015-24

Created in TradingView

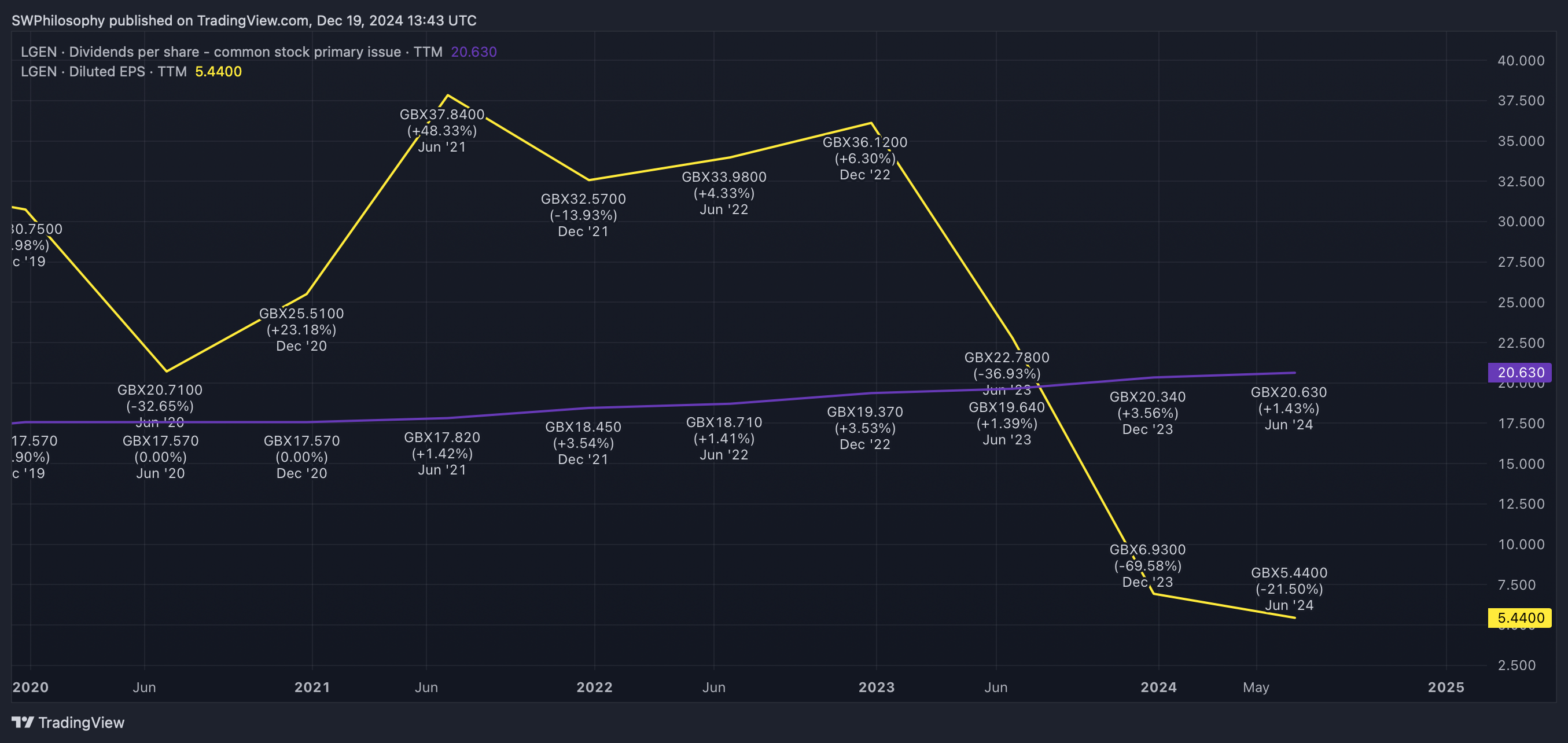

Management anticipates a 2% annual increase in the dividend with additional cash to be distributed through share buybacks. But investors might initially wonder how Legal & General is going to finance this.

Currently, the company pays more to shareholders than it generates as net income. But while this may seem like a cause for concern, it's probably less of a risk than it initially appears.

Statutory and general dividends per share vs. earnings per share 2020-24

Created in TradingView

At the end of 2023, Legal & General has more than £9 billion of excess capital after meeting its solvency capital requirement. This should mean that the company can meet its ongoing dividend commitments.

Perspective

In terms of future growth, Legal & General's main driver is its Pension Risk Transfer business. Assumes future guaranteed pension obligations from other companies, in exchange for a commission.

Management is optimistic about the pipeline of new deals in the coming years. But investors must be clear that both quality and quantity are present.

Getting cash up front before paying costs later is a good structure. But the deals have an asymmetric risk structure: the amount Legal & General can earn is fixed, while the potential liabilities are not.

Even including the returns the company can generate by investing the premiums, it will be a long time before the profitability of the contracts becomes clear. And this is where the risk for investors comes from.

A no-brainer?

As an investment, Legal & General stock is anything but a no-brainer. The nature of the company's potential liabilities means that there is a lot of uncertainty about the future, especially in the long term.

That's why the dividend yield is so high: investors need something that gives them a margin of safety against current risks. While 9.3% might be enough for some, I'm looking elsewhere.

{kind=link}