Image source: Getty Images

Scottish Mortgage Investment Trust (LSE:SMT) is proud to have found the next winning growth stock. But this approach comes with quite a bit of volatility.

For proof, look at Scottish Mortgage's share price, which is up 41% in the last 18 months but still remains 37% lower than its 2021 high.

when he S&P 500 and Nasdaq Both reach new heights almost daily, which has been a bit frustrating for many shareholders (myself included).

Granular data

Perhaps that is why there has been a notable effort by management to increase commitment to shareholders. More interviews, webinars, updates, ideas, that kind of thing.

There was even an October lunch interview with senior manager Tom Slater at The timeswhere we learned that he likes eggplant involtini and uses a smart mattress to track his sleep.

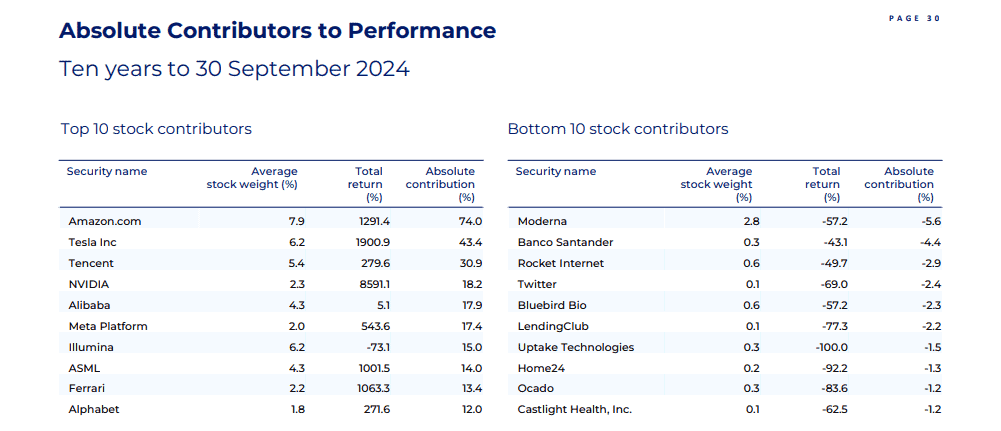

Recently, Scottish Mortgage also released a quarterly data package, which provided shareholders with an under-the-hood peak at portfolio returns. I think there was some interesting information there that demonstrates the power of long-term investing.

A failure of the FTSE

Currently, only 3% of the trust's assets are in UK shares. one of them is ocado (LSE: OCDO), the online grocery and robotics company.

According to third quarter data, the trust's investment in it had fallen 83.6% in the five years to September 30. Oh.

In hindsight, we can see that investing in Ocado in 2020 during the peak of the pandemic-driven online grocery boom was crazy. It has since gone downhill and post-Covid conditions have normalized, along with Ocado's growth rates.

The company has even been downgraded from blue-chip status. FTSE 100 after his spectacular fall. The problem comes down to profits or lack thereof. In the first half of 2024, it reported a pre-tax loss of £154m.

I had a brief brush with the stock a year ago, opened a small position and then ran for the hills when the CFO said it would be someone else's turn.”six years”(!) before the company expected to make a pre-tax benefit.

A risk here is that Ocado will need to turn to shareholders for more money at some point. After all, the high-tech robotic warehouses it builds in partnership with the world's leading grocery stores aren't cheap.

That said, Ocado has been the fastest growing supermarket in the UK in recent months, while its robotics business still has exciting potential. However, I will not be investing and would prefer to gain exposure through Scottish Mortgage's involvement (what's left of it).

Asymmetry in action

For every handful of Ocados that fall more than 80%, the trust has hit the jackpot with a big winner.

We saw it in the data package, which confirmed that what is at stake in NVIDIA and tesla had obtained a return of 2,475% and 1,415%, respectively, in five years. Nice.

Over 10 years, the asymmetric returns were even more pronounced. The trust was based on five '10-baggers' (10x returns). These were Nvidia (actually an 85-bagger!), Tesla, amazon, ASMLand ferrari.

It is these outliers that have helped Scottish Mortgage achieve a return of 347% over the last decade, surpassing the 211% produced by the FTSE everyone index.

The risk is that managers will fail to identify the next generation of massive stock market winners. But looking at the portfolio today, I'm optimistic that they are in there somewhere, ready to generate more gains.

{kind=link}