Image source: Getty Images

Even a solid FTSE 100 stocks with a strong balance sheet, modest valuation, generous yield and solid earnings prospects can take a beating, as a homebuilder. Taylor Wimpey (LSE: TW) is showing it to us right now.

The Taylor Wimpey share price has plummeted 17.73% over the last month. I maintain the action and I am suffering. In 12 months, it has increased only 2.77%.

I bought Taylor Wimpey shares three times last year and for a while they were a hit. I went up more than 40% and also got a return of 7%. Then everything went wrong.

Why are stocks falling?

I bet a lot on Taylor Wimpey because I was impressed with how its balance sheet and share price remained relatively strong during the pandemic and cost of living crisis.

While revenue inevitably fell in 2020, it quickly recovered. They fell again in 2023, but investors held on in the hope that inflation and interest rates would eventually follow, making mortgages much cheaper.

On Nov. 7, the board endorsed its full-year 2024 outlook as demand and affordability improved. It hoped to hit the top end of its target of building between 9,500 and 10,000 new homes, with an operating profit in line with current market expectations of £416m.

That was down from £473.8m in 2023 amid fewer completions, but the order book grew from £1.9bn to £2.2bn, excluding joint ventures.

However, the October 30 budget was painful. Chancellor Rachel Reeves' decision to charge employers with extra national insurance contributions worth £25bn will reduce Taylor Wimpey's margins. They are expected to fall from 13.3% to 12% next year. A shortage of skilled workers can also drive up wages.

Furthermore, the Bank of England forecasts the Budget will push inflation back up to 3% in 2025, and mortgage lenders are raising rates.

I will maintain split income and expect growth.

US President-elect Donald Trump's policies are also expected to be inflationary, raising concerns about interest rates. Higher inflation will also increase Taylor Wimpey's input costs.

On another note, Labour's plans to build 1.5 million homes in five years look a bit hopeful. Ironically, that may support Taylor Wimpey, by limiting property supply at a time of sky-high demand.

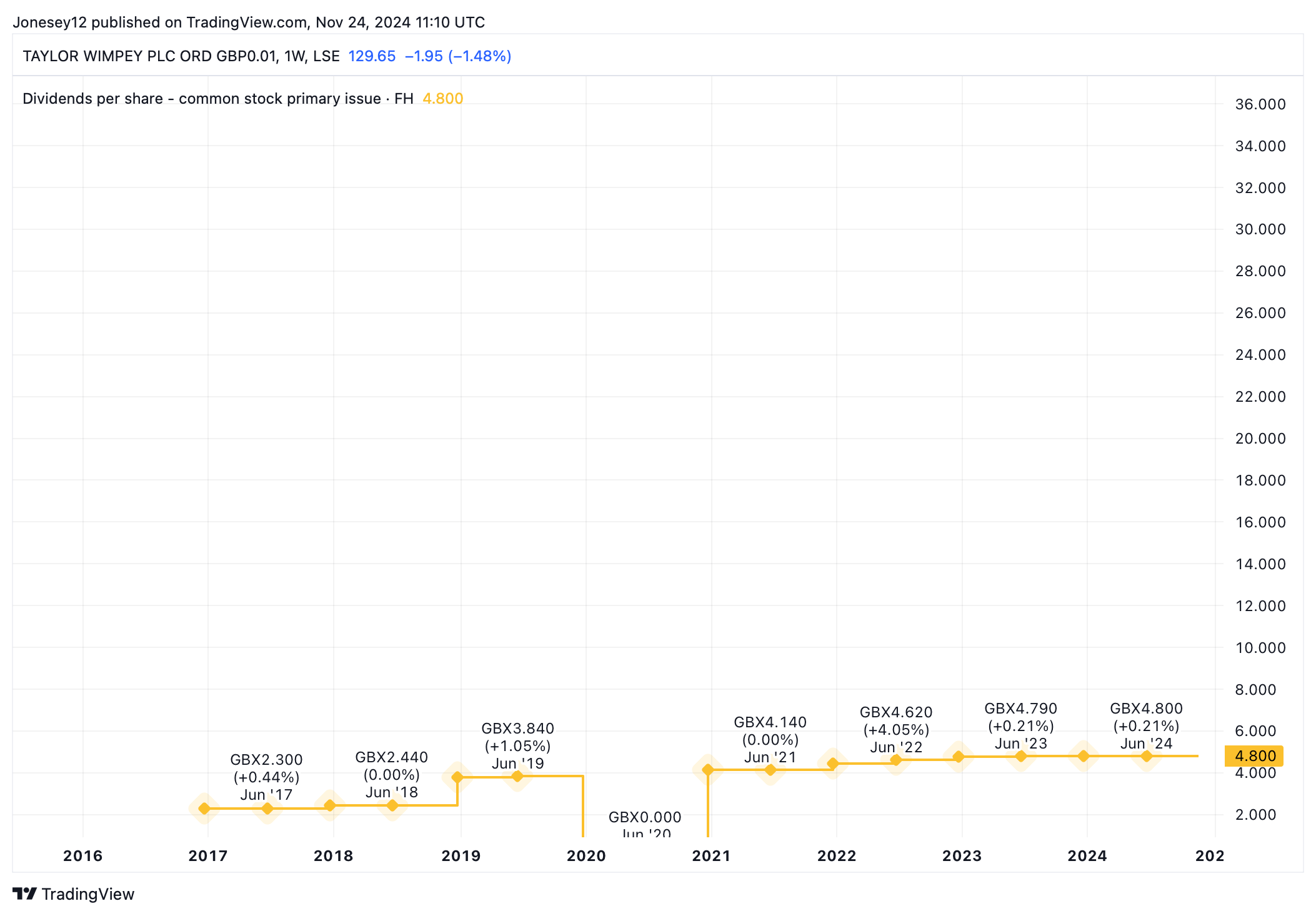

The shares strike me as fair value, trading at 12.8 times earnings. This is still an excellent dividend income stock. The 2024 return is 7.34% and analysts expect it to reach 7.56% in 2025. Its track record is reasonably strong, as this chart shows.

Chart by TradingView

The 16 analysts offering one-year share price forecasts have set an average target of 167.65p. If that comes true, it will increase by 29.32% from today. Which would be brilliant.

Interestingly, there is not such a wide range of recommendations. An impressive 12 calls Taylor Wimpey a Strong Buy, two say a Buy and two say Hold. None suggest selling. I'm certainly not considering it myself. I would also label it a Strong Buy.

If I didn't already have a large stake, I would take this opportunity to buy more with a long-term view. Britain needs houses and I think I need dividend growth stocks like Taylor Wimpey.

{kind=link}